Yields and Credit Quality Make High Yield Bonds Attractive for 2025

We expect high yield bond credit spreads to stay rangebound below the long-term average in 2025, driven by strong fundamentals, supportive technical trends and attractive yields.

Corporate fundamentals are stabilizing but they remain strong relative to historical levels. Leverage continues to sit below historical averages while interest coverage ratios remain above average. As a result, credit ratings upgrades are outpacing downgrades. The net result is the composition of the high yield market remains close to the highest quality since inception.

Looking ahead, we expect companies to maintain better-than-average balance sheets given funding costs are higher than the decade before the pandemic. Recent economic drivers such as the artificial intelligence boom have dramatically impacted some of the previously distressed segments in the market. As a result of these fundamental drivers, the percentage of distressed companies continues to decline, which bodes well for maintaining future low default rates. Combined with strong balance sheets, default rates are likely to remain well below the 4% historical average.

The technical picture in high yield remains supportive. After two years of contraction in 2022 and 2023, the high yield market is on track to expand slightly in 2024. Issuance picked up this year as financing costs normalized and are close to current yields. However, net issuance remained low as companies maintain a conservative stance and focus on refinancing rather than re-leveraging. On the demand side, inflows for the asset class have been strong as investors look to lock in attractive yields. Against a backdrop of expected continued monetary policy easing, we believe the trend of refinancing activity will remain a primary driver of issuance. The decline in interest rates and a more constructive macro outlook could drive a potential pickup in merger and acquisition activity, which could lead to a slight uptick in net issuance.

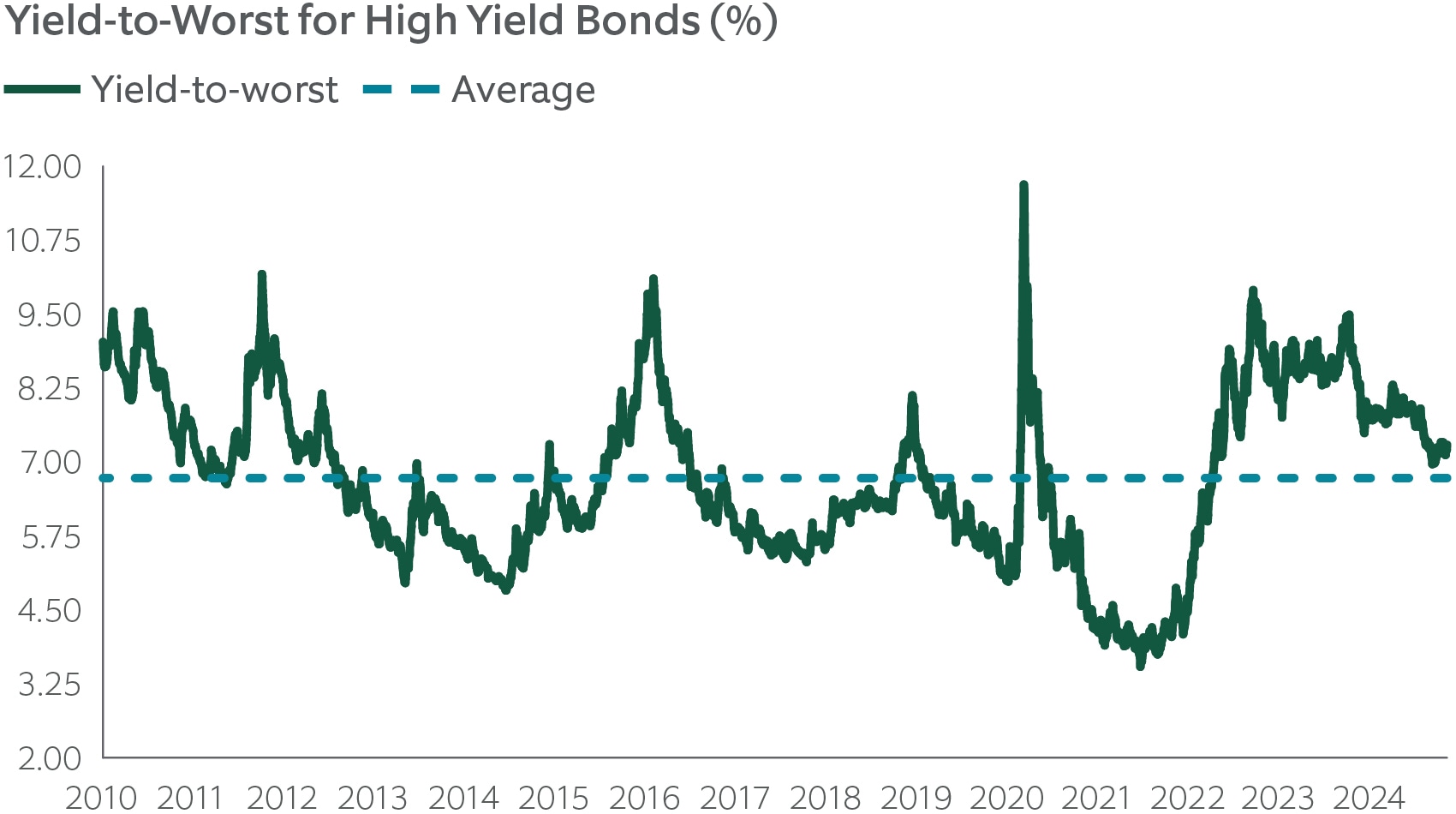

Valuation remains favorable in the high yield market. The starting yield of 7.29% (as of November 15, 2024) is among the highest since the Global Financial Crisis period (2007–2008) and supports attractive returns. Our expectation of low defaults and a supportive Federal Reserve are positive for investors seeking total returns with reduced volatility compared to other risk assets. Credit spreads, on the other hand, are at the lower end of the historical range. We believe it could widen slightly, while likely staying rangebound. However, we think any likely losses will be manageable due to the high yield market’s record low duration and would be easily absorbed by current yields.

Exhibit 1: Attractive Yields

Above-average yields, combined with historically high credit ratings in the high yield market, support a strong outlook.

Source: Bloomberg. Daily yields from January 1, 2010 to November 15, 2024. Yield-to-worst is the yield on a callable bond (where the issuer may pay off a bond before its maturity date) that assumes a bond is called at the earliest opportunity. Yields are annualized interest (coupon) payments divided by the bond market price. Historical trends are not predictive of future results.

Main Point

Attractive Outlook for High-Yield Bonds in 2025

We think favorable financial conditions for issuers and above-average yields make high bonds attractive for 2025. We expect credit spreads to remain rangebound.