WHY IT PAYS TO CLIP COUPONS

MAY 14, 2018

A rising rate environment means the majority of fixed income investors’ return in 2018 is likely to come from carry or yield and not from price appreciation. Brandywine Global's Brian Kloss sees careful selection of higher yielding securities as the key for returns and protecting valuations.

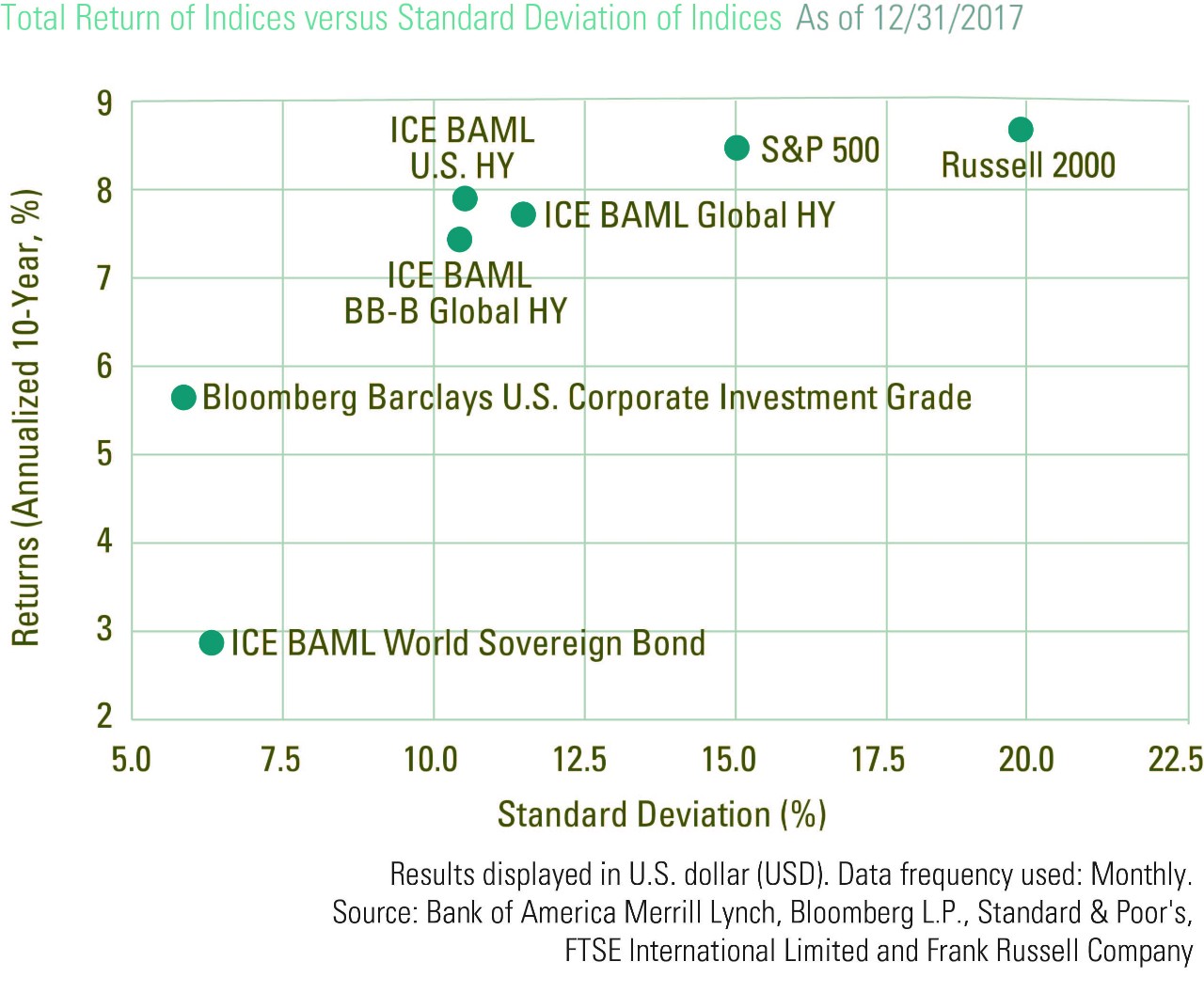

Two of the biggest risks in 2018 come from the interest rate sensitivity of high quality instruments and from the impact of tightening on US high yield debt. However, a 10-year government bond is going to have much greater interest rate sensitivity than a corporate bond that matures in 2020 or 2021. While assessments from our proprietary models show U.S. high yield debt is around fair value after massive spread compression between 2009 and now.

Furthermore, it is our view that in 2018 the majority of potential return is going to come from carry or yield and not from price appreciation. So, this might not be the best time to dial down exposure to high yield. However, debt issued by higher leveraged companies is at risk from downgrades or rising defaults as rates rise. Therefore a move up in quality and taking a more conservative and defensive stance looks sensible. Security selection will be very important.

In selecting securities, we see business models that have strong management teams, significant asset protection and the ability to weather the next recession as attractive. They are even more attractive where our fundamental analysis shows the debt issued by these companies to be worth a BB credit rating, when the official rating is only a single B.

An added uplift in the high yield space is the potential for a fairly robust mergers and acquisition market. It is our belief that a lot of investment grade companies will be looking to acquire assets at below investment grade companies with good balance sheets. Steel companies, healthcare companies and energy companies are all likely targets. Here, spreads will come down for such bonds once a merger target is announced.

Another opportunity comes from a trend we have observed where lower quality credits do well in the first part of a tightening cycle. This is significant as we expect the normalisation of rates to be a very slow process; we are of the view that there will be only three rate hikes this year and not four. Furthermore, global growth is still at 2-3% and this is a conducive environment for credit instruments. While tax cuts in the US probably means that small caps and more domestic focused companies can do well. Later in cycle as you move towards the likelihood of a recession the risk grows.

Author:

Brian Kloss, JD, CPA

Portfolio Manager

Originally Published at: WHY IT PAYS TO CLIP COUPONS

The opinions and views expressed herein are not intended to be relied upon as a prediction or forecast of actual future events or performance, or a guarantee of future results, or investment advice.

Commodities and currencies contain heightened risk that include market, political, regulatory, and natural conditions and may not be suitable for all investors.

IMPORTANT INFORMATION: All investments involve risk, including loss of principal. Past performance is no guarantee of future results. An investor cannot invest directly in an index. Unmanaged index returns do not reflect any fees, expenses or sales charges.

Equity securities are subject to price fluctuation and possible loss of principal. Fixed-income securities involve interest rate, credit, inflation and reinvestment risks; and possible loss of principal. As interest rates rise, the value of fixed income securities falls. International investments are subject to special risks including currency fluctuations, social, economic and political uncertainties, which could increase volatility. These risks are magnified in emerging markets .

The opinions and views expressed herein are not intended to be relied upon as a prediction or forecast of actual future events or performance, guarantee of future results, recommendations or advice. Statements made in this material are not intended as buy or sell recommendations of any securities. Forward-looking statements are subject to uncertainties that could cause actual developments and results to differ materially from the expectations expressed. This information has been prepared from sources believed reliable but the accuracy and completeness of the information cannot be guaranteed. Information and opinions expressed by either Legg Mason or its affiliates are current as at the date indicated, are subject to change without notice, and do not take into account the particular investment objectives, financial situation or needs of individual investors.