Volatility Skew and Term Structure: Week of May 15

Volatility has lost its mind. Just the other week the VIX was nearing all time lows, shrugging off political news and then a week later we see a 46.6% VIX spike in a single day on very similar news! Let’s break all this movement down...

This VIX is generally a reflection of hedging and options activity on the S&P 500 and when the VIX was near all time lows, it would appear that market participants have significantly decreased their downside protection. But something occurred that does not happen very often. The VIX and the VVIX diverged over a 7 day period. This is always an interesting phenomenon to observe because it signals investors utilizing the VIX options directly to hedge their positions (as measured through the VVIX) or investors taking a directional shot at the market. As we know know, that was one hell of a trade.

To get a full sense of what is happening in the S&P options market and hedging activities, it’s important to look at both the VIX and VVIX to get the full picture. While on the surface it may appear that market participants were being complacent, there was still a flurry of trading activity going on directly with VIX options.

So what about that 46.6% spike in the VIX? It was the the 5th largest daily spike the VIX has ever had. To make matters more interesting, the skew in the options market is still relatively steep. A steep skew is a general indication of a sideways to bullish market. So although the at-the-money volatility has dramatically increased on Tuesday and skew flattened out a little, it is still a touch on the steep side, especially for the spike in volatility that we just saw.

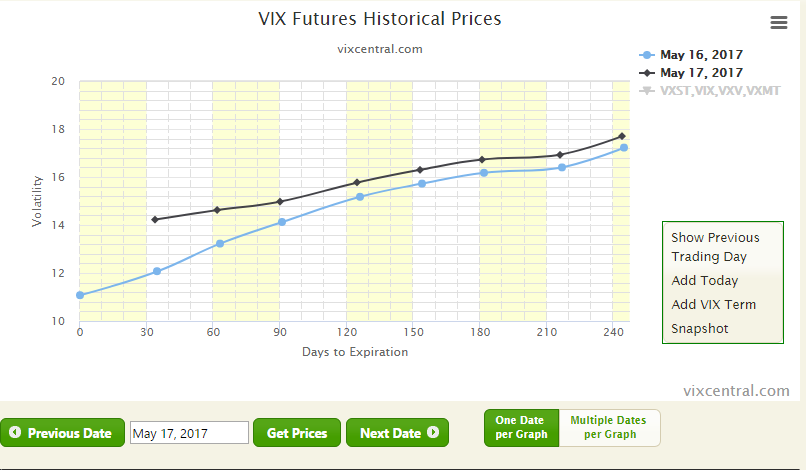

Looking at other months on the horizontal skew curve or term structure (similar to futures or bond term structure) the VIX curve is still in contango, another sign of a sideways to up trending market. While the front of the curve flattened out slightly from the large spike in volatility, the back months had a relatively small effect.

So what does all of this mean for options spread traders? If you are a seller of volatility, then last Wednesday provided a great opportunity to reposition your trades and take advantage of the spike in vol. While skew started to flatten out a little, certain spread traders enjoyed cheaper pricing but still need to be cautious of a potential strong market rebound.

For equity investors, keep a watch on the VIX term structure (vixcentral.com) over the next week or so. A flip to backwardation at more than 60 dte and a continued flattening of the skew curve can indicate bumpy markets ahead.

The Blackpier Team