“That’s Our Two Satoshis” - Crypto Market Recap October 16, 2018

What happened this week in the Crypto markets?

A tale of two explanations

First, let’s state the obvious. It was not a good week for owners of risk. From global equity markets (-4-7%) to the VIX (+40%) to Gold (+2%) to Oil (-4%) to Bitcoin (-6%) and even US Treasuries (+0.3%)... it was a pretty clear “risk off” week for most global market participants amidst an old-fashioned “flight to quality” trade. These coordinated market moves were not too dissimilar to those seen in Feb-Mar 2018, albeit on a smaller and shorter scale (from Jan 27, 2018, to March 22, 2018, US equities fell 10% over a 2-week span, BTC fell 35%, and the VIX spiked almost 300% before retreating).

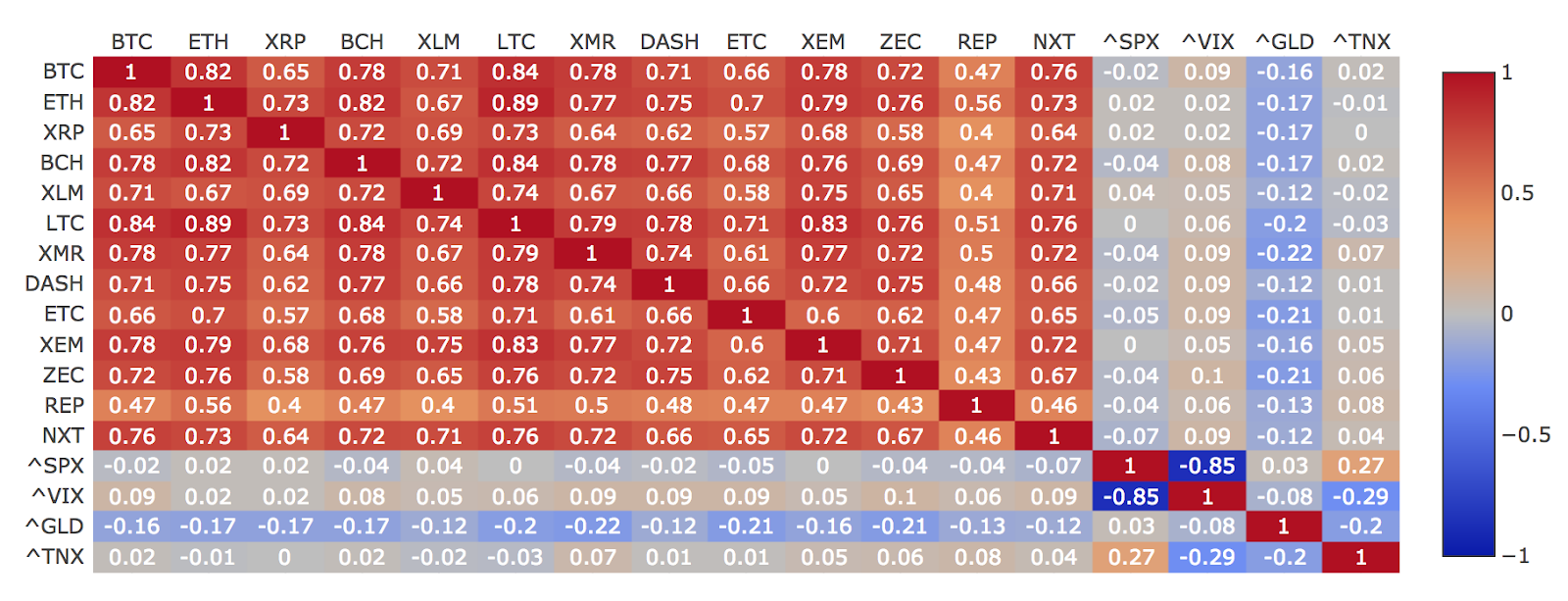

While crypto markets have historically been very uncorrelated to other asset classes and markets, with the exception of recent correlations with Asia and emerging markets , we still believe it is critical to look across the world for clues into general market sentiment and avoid the narrow lens with which crypto is often viewed. So as global markets sold off Wednesday and into Thursday, the question for those of us studying, and investing in, the crypto markets is two-fold:

-

Why did BTC (-6%) and the rest of the crypto market (-11%) get swept up in this selloff when it is supposed to one day be perceived as a “safe haven” asset class?

-

Why was there a lag effect (crypto experienced a 13% “flash crash” in a 2-hour span several hours AFTER US markets closed Wednesday and before Asian markets opened on Thursday)?

Cryptocurrency Correlation Matrix (Rolling 180 days) shows low correlations to other markets

Source: Sifr Data

In hindsight, two explanations emerged to describe the crypto panic, both of which are plausible, but neither of which was widely discussed before the crypto selloff:

-

Correlation often goes to 1.0 across all risk assets during market turmoil, and thus, there are no true “safe havens”.

-

This had nothing to do with equities or emerging markets but instead was due to fear of failures at one of the largest exchanges (Bitfinex) and one of the highest volume stablecoins (Tether USDT).

Here’s the thing. It doesn’t really matter what caused the crypto sell-off if narratives are always being created after events happen, instead of price action following market narratives that were already created.

While the global equity market selloff may have been swift and violent, you certainly couldn’t call it “unexpected”. There have been risks piling up for years caused by low-interest rates, government intervention, and massive personal, corporate, and government debt accumulation. Throughout this time, there has been no shortage of market hypotheses stating that when rates finally begin to rise, and the central bank stimulus begins to be withdrawn, the “everything bubble” will unwind . Of course, only time will tell if this recent hiccup in global equities is the start of a much larger drawdown , or an opportunity to “ buy the dip ”. But the narrative has been established - rising rates and stimulus withdrawals are huge headwinds to global stocks.

Which brings us back to crypto. The only persistent narrative in recent months has been the downfall of ICOs but the subsequent pickup in blockchain equity raises , and the constant influx of Fortune 500 companies into crypto . There were no calls for a “correction” in crypto prices outside of normal short-term technical analysis, and the persistent “ crypto is going to zero ” Twitter banter (which has been going on since Bitcoin was below $100). Last week’s move really did catch the market by surprise. And in our opinion, that’s fine. Not every move needs to be associated with a reason, which is why we continue to shout about proper risk management over everything else. The entire crypto space consists of new technology that probably should not offer real-time pricing and liquid exchanges. There are long periods of inactivity on many newly built protocols and platforms that underpin the tokens that trade, and each blockchain startup and decentralized project comes with plenty of development and network hiccups. If every private company in Silicon Valley gave daily, transparent updates into their company’s financial health or future business plans, their equity would move up and down in 10% increments as well. And you wouldn’t require a reason - it would just be par for the course when investing in young companies and emerging technologies.

Crypto should be part of an overall balanced portfolio

Perhaps more importantly, NONE of these markets should be viewed in isolation. The whole point of having a diversified portfolio made up of positions in a lot of different asset classes across different markets is to shield investors from any one specific outlier, good or bad.

So even if you are prescient and had moved to 100% cash ahead of this recent downturn, keep in mind you are still 100% long the banking and financial system. Market risk may be removed, but systemic risks don’t go away as you are still sitting within the global banking system. And as we saw in 2008 (banking), 2011 (Euro sovereigns) and now in 2018 (EM crisis), we continue to find ourselves in situations that advocate for having some allocation outside of the traditional banking system. Despite last week’s correlation, crypto still offers the best hedge against these shocks.

Notable Movers and Shakers

There weren’t a lot of token-specific catalysts this week, as most tokens moved in line with the overall market selloff. There were, however, a few noteworthy exceptions:

-

0x (ZRX) only dropped 4% week-over-week after a 30% one-day spike (Thursday) offset earlier losses following news that Coinbase Pro will list and allow trading in 0x and 0x pairs. This is the first ERC20 token that Coinbase has supported. While the announcement of new listings on most exchanges/platforms no longer moves markets, this demonstrates how important Coinbase still is in this ecosystem.

-

GoChain (GO) jumped 21% on Saturday and ended the week +26%. This followed a report from Bitcoinist labeling GO as one of the best token investments.

-

Tether (USDT) fell ~3-10%, depending on where you look. This is a big deal as USDT is supposed to maintain a 1:1 USD peg, so any move below $1.00 is a disheartening discount to NAV. Fears continue to spread that Tether is not actually backed dollar for dollar by US fiat, which is having ripple effects across the market. Ironically, in an ecosystem designed to avoid centralization and single points of failure, we may be looking at an old-fashioned bank run as a large arbitrage now exists between selling USDT at Bitfinex compared to every other exchange.

What We’re Reading this Week

Funds Are Using Back Door for Crypto Buys

We’ve mentioned before that the OTC market continues to be an important influencer in crypto, and this article does a nice job shedding some light on this marketplace, including legal reasons why some funds are targeting specific newly mined coins.

Bitfinex may have partnered with HSBC

Long story short, Bitfinex and Tether lost its banking partner (Noble Bank), which appears to be heading towards insolvency if it’s not purchased. As mentioned above, the effects on the stabletoken, Tether (USDT), and the exchange, Bitfinex, have led the market to massive withdrawals. If this relationship with HSBC proves true, this will help stabilize market fears.

Upending our Legacy financial system

If you only read one educational piece on why decentralization and blockchain matter, read this.

Goldman Is Looking to Reduce Marcus Lending Goal on Credit Caution

A low growth, high-interest rate, weak credit economic cycle is a recipe for disaster, and this revision reflects concern about the stage of the credit cycle and changes in market data.

Real use-cases: Forbes is trying out the blockchain

Many publishers are skeptical of introducing blockchain technology into their supply chains because it’s new and it’s difficult to understand. Forbes is sending a message to the industry that they think blockchain for journalism is the future.

PODCAST: Barry Silbert on What Wall Street Says Privately About Crypto Vs. What It Says Publicly

Barry Silbert, CEO of DIgital Currency Group, gives a great overview of crypto as a VC investment and as an infrastructure underpinning all existing asset classes.

Arca in the Press & on the Streets

-

Arca’s CEO Rayne Steinberg spoke at Blockcon last week , discussing the future of crypto and how blockchain fits into traditional portfolios as an investable asset class.

Arca Funds’ Portfolio Manager, Jeff Dorman, is speaking on the “ Blockchain as an Asset Class ” panel at the upcoming CalALTS event in Los Angeles on Thursday, Oct 18th.

And That’s Our Two Satoshis!

Thanks for reading everyone! Questions or comments, just let us know.

- The Arca Portfolio Management Team