TAKE A BREAK, MR. POWELL

DEC 20, 2018

We believe the Fed should pause and acknowledge that what it's done so far is affecting the economy – perhaps more than stated so far.

All eyes were on the Federal Reserve (Fed) this past week—not so much on what it did, but on what Chairman Powell suggested may guide its actions in the future.

After the December rate hike, we believe the Fed should pause and acknowledge that what it has done so far is having an effect on the economy – and may be more potent than it has acknowledged so far.

Chairman Powell and Vice Chair Clarida have recently hinted that the fed funds rate may be reaching the neutral zone, which is somehow embedded in their R* concept. Raising the fed funds rate far enough so it can be lowered in the next downturn seems like a perfect attitude to create the next downturn.

Francis Scotland has written cogently on the risks never defined by the Fed in the quantitative tightening (QT) program which is draining liquidity from the system late in the cycle. This piece presents an idea that may give the Fed an “Aha” moment that it has reached neutral or beyond.

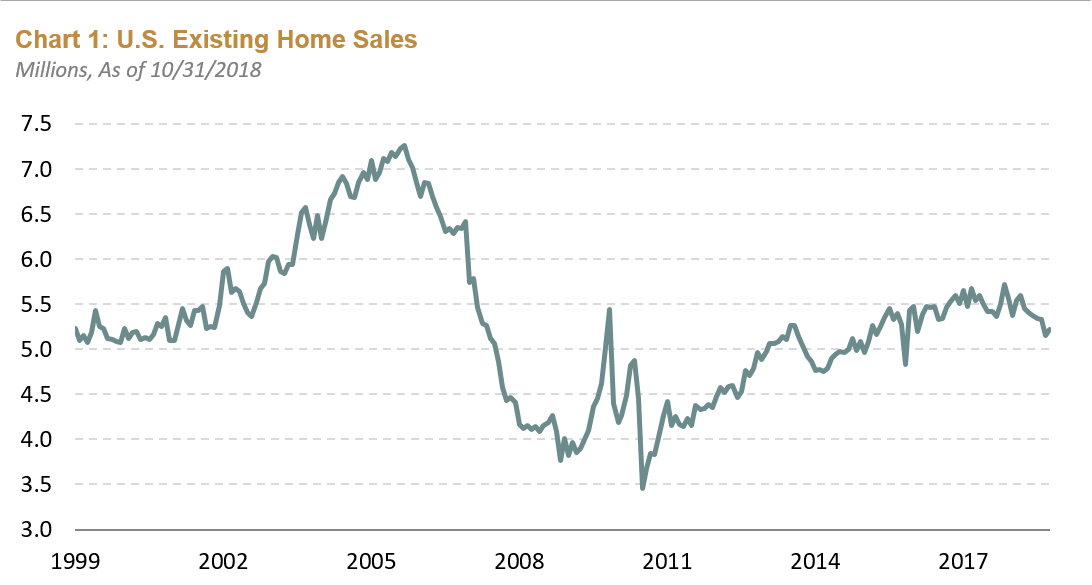

In plain sight

Conducting economic analysis by simply looking around can tell us some important things. Housing has begun to roll over, and is commonly thought of as the most interest-rate sensitive part of the economy. While rates are still low in a Post-War construct, they have moved up considerably, raising the cost of purchase and lowering prices. Consider this the “canary in the coal mine.”

Chart Courtesy of Brandywine Global Investment Management. Source: Macrobond, as of 10/31/2018. Past performance is no guarantee of future results. This information is provided for illustrative purposes only and does not reflect the performance of an actual investment.

The Fed’s dual mandate targets inflation and full employment. While my blog addresses the fed funds rate through the lens of inflation, unemployment at 3.7% seems to be a real concern. This comes after the average worker has experienced a decline in real income for 20 years! The Phillips curve seems to have lost its relevance, not only in the U.S., but around the developed world. Productivity is finally rising. Why is it the Fed’s job to keep wages down for the average worker?

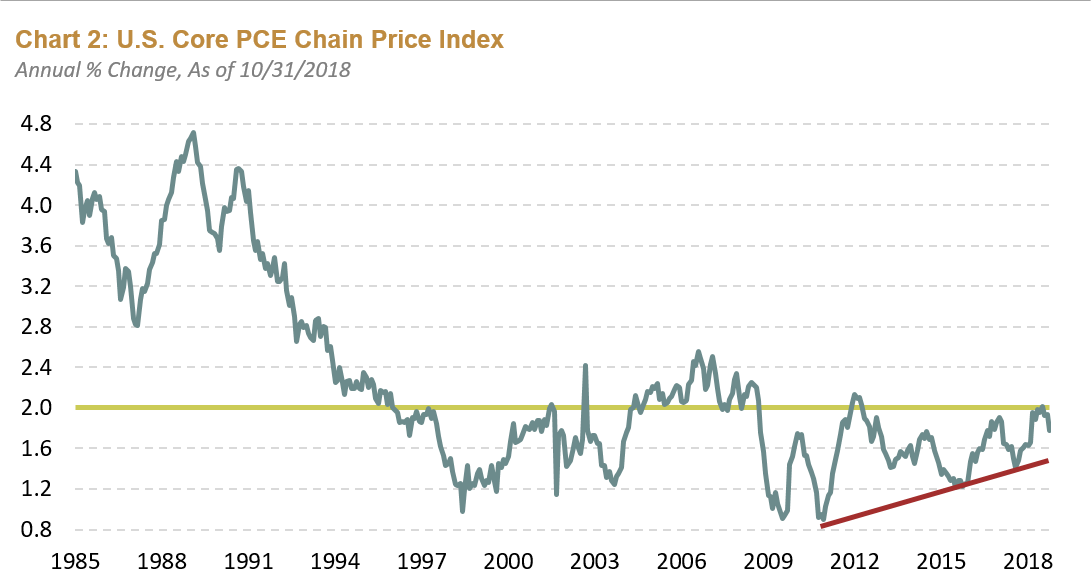

The inflation equation

The core personal consumption expenditures (PCE) deflator is the Fed’s stated favorite inflation target. Chart 2 below shows that the Fed has reached its target, and now the PCE deflator seems to be heading down.

Chart Courtesy of Brandywine Global Investment Management. Source: Haver Analytics, as of 10/31/2018. Past performance is no guarantee of future results. This information is provided for illustrative purposes only and does not reflect the performance of an actual investment.

The numbers falling off from last year show that 1.5% is a real possibility. Why is the Fed ignoring this? Vice Chair Clarida stated that the Fed might be comfortable with inflation above its target for a period of time, even as it falls, while market-based indicators like the 5-year breakeven inflation rate derived from the Treasury market has collapsed from 2.1% to 1.6% since Chairman Powell’s speech on October 2, when he stated the neutral rate was far away. He did not state whether far away meant time or level, but the markets have been concerned since. The PCE deflator has spent most of the time below 2% since 1995. Why is the Fed ignoring the fact that the PCE deflator only touched 2% and has moved into reverse?

Maybe the secret to understanding the Fed is that it seems to be grounded in absolute levels, while the market—and I believe the world—is more affected by relative price changes. Also, demographics, debt levels, and technology all have an impact on inflation, and all exert some degree of downward pressure.

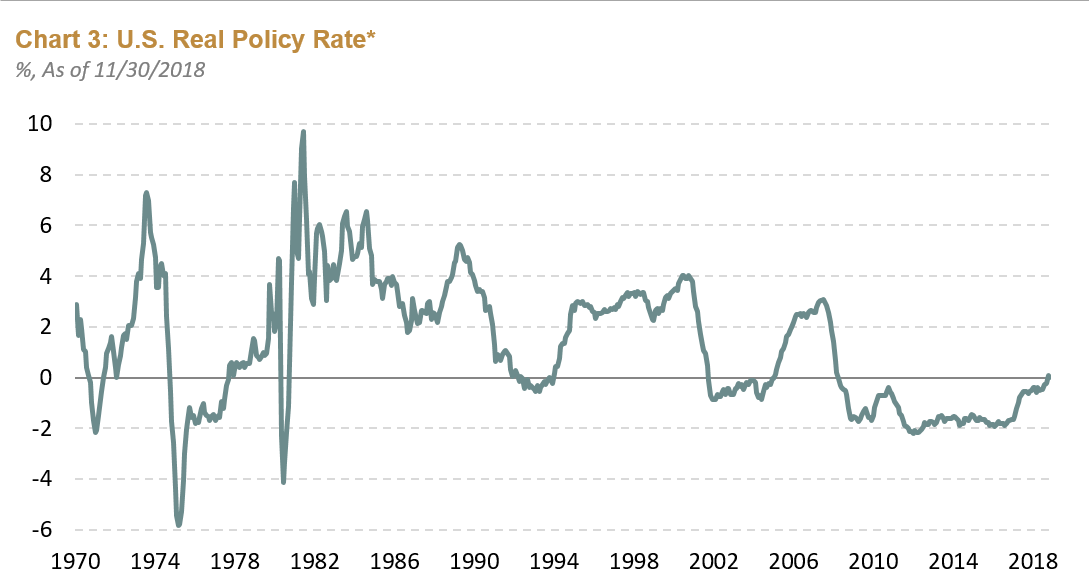

The real deal

The next two charts show two ways at looking at the changes in the real fed funds rate over time. The first (Chart 3) is simply the real rate that has been in a downtrend since Paul Volcker broke the back of inflation as Fed Chairman in the early 80s.

Chart Courtesy of Brandywine Global Investment Management. Source: Haver Analytics, as of 10/31/2018. * The policy interest rate refers to the Fed's target rate, and is adjusted for inflation using the U.S. Core PCE Price Index. Past performance is no guarantee of future results. This information is provided for illustrative purposes only and does not reflect the performance of an actual investment.

The real rate has reached zero, much higher than recent history, but perceptibly low by many Federal Open Market Committee (FOMC) members, who see a dot plot moving higher into more historically normal levels. I believe, as do the markets, that this is a risky strategy, which could lead the Fed to over-tighten again after creating the risks in the first place.

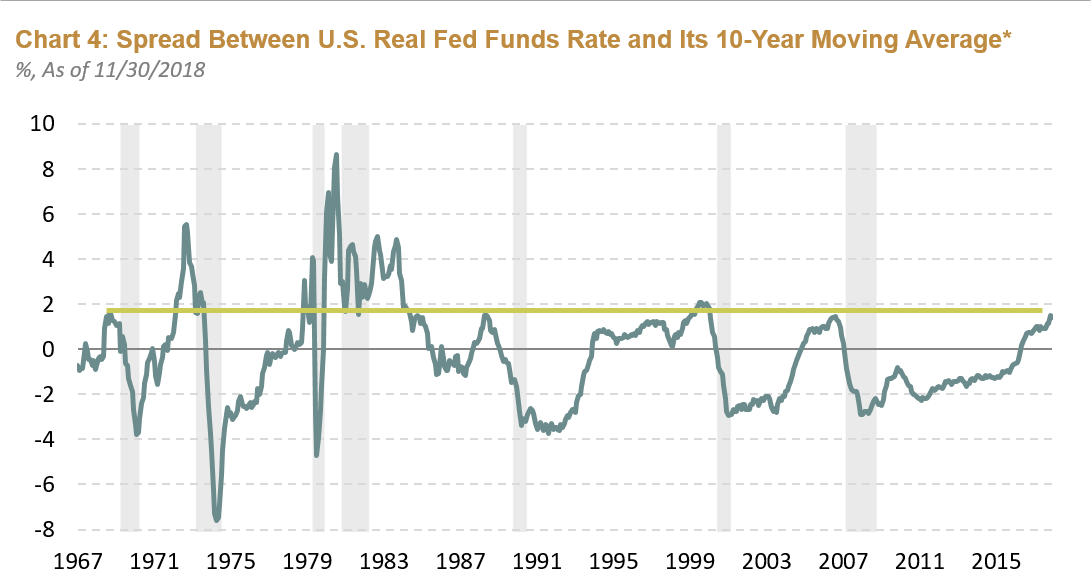

By any sensible thinking, Chart 3 shows the real funds rate is very low. However Chart 4 gives a completely different interpretation, and gives an invitation to the Fed to pause after the inevitable hike on December 19. The Fed should take the pause that refreshes, and wait patiently and observe.

Chart Courtesy of Brandywine Global Investment Management. Source: Haver Analytics, as of 10/31/2018. * The policy interest rate refers to the Fed's target rate, and is adjusted for inflation using the U.S. Core PCE Price Index. Past performance is no guarantee of future results. This information is provided for illustrative purposes only and does not reflect the performance of an actual investment.

Be careful what you fear

If we think about history, we see that the real funds rate is up meaningfully relative to its 10-year average. So what? You can observe that with the exception of two occasions—both periods of embedded inflation expectations and an oil crisis to boot—a recession followed in the not-too-distant future after reaching this current spread. It is because this spread translates into economic change through higher rates hitting housing, putting downward pressure on price-to-earnings for the stock market, increasing real corporate borrowing costs, and putting upward pressure on the U.S. dollar. The interest rate side of the Fed’s mandate is saying loudly to take a break. The Fed can always tighten again if needed. Why create what you most fear?

Author:

David F. Hoffman, CFA

Managing Director, Portfolio Manager

Definitions

The Phillips Curve is an economic concept developed by A. W. Phillips stating that inflation and unemployment have a stable and inverse relationship.

The Federal Funds rate (Fed Funds rate, Fed Funds target rate or intended Federal Funds rate) is a target interest rate that is set by the FOMC for implementing U.S. monetary policies. It is the interest rate that banks with excess reserves at a U.S. Federal Reserve district bank charge other banks that need overnight loans.

“R-star” or r* refers to the real short-term interest rate expected to prevail when an economy is at full strength and inflation is stable, according to economic models described in studies by Laubach-Williams (“LW”) and Holston-Laubach-Williams (“HLW”)

Quantitative easing (QE) refers to a monetary policy implemented by a central bank in which it increases the excess reserves of the banking system through the direct purchase of debt securities. Quantitative tightening (QT) refers to policies design to reverse the flow of central bank reserves, reducing the excess reserves by selling from their inventories of debt securities.

The Personal Consumption Expenditures (PCE) Price Index and the PCE Deflator are measures of price changes in consumer goods and services; the measures include data pertaining to durables, non-durables and services. This index takes consumers' changing consumption due to prices into account, whereas the Consumer Price Index uses a fixed basket of goods with weightings that do not change over time. Core PCE excludes food & energy prices.

The “dot plot” refers to a graphic representation of the forecasts of the members of the Federal Reserve’s Open Market Committee (FOMC) with respect to interest rates, growth and employment.

IMPORTANT INFORMATION: All investments involve risk, including loss of principal. Past performance is no guarantee of future results. An investor cannot invest directly in an index. Unmanaged index returns do not reflect any fees, expenses or sales charges.

Equity securities are subject to price fluctuation and possible loss of principal. Fixed-income securities involve interest rate, credit, inflation and reinvestment risks; and possible loss of principal. As interest rates rise, the value of fixed income securities falls. International investments are subject to special risks including currency fluctuations, social, economic and political uncertainties, which could increase volatility. These risks are magnified in emerging markets .

The opinions and views expressed herein are not intended to be relied upon as a prediction or forecast of actual future events or performance, guarantee of future results, recommendations or advice. Statements made in this material are not intended as buy or sell recommendations of any securities. Forward-looking statements are subject to uncertainties that could cause actual developments and results to differ materially from the expectations expressed. This information has been prepared from sources believed reliable but the accuracy and completeness of the information cannot be guaranteed. Information and opinions expressed by either Legg Mason or its affiliates are current as at the date indicated, are subject to change without notice, and do not take into account the particular investment objectives, financial situation or needs of individual investors.

Forecasts are inherently limited and should not be relied upon as indicators of actual or future performance.