Seizing the Opportunity in Emerging Markets

With attractive valuations, emerging market equities look like a good opportunity. A factor investing strategy, designed well, may enhance performance and help manage some key risks.

Point of View 9.11.24

Key Points

What it is

Attractive valuations may brighten the outlook for emerging market equities, especially if supported by factor investing.

Why it matters

There may be significant upside in emerging markets after years of lagging performance.

Where it's going

Thoughtful and purposeful factor-based strategies can provide emerging markets investors with opportunities to improve their investment outcomes.

Investors have long sought attractive returns and diversification by allocating to emerging markets. However, their recent underperformance compared to developed markets has sparked worries about whether investing in emerging markets is worthwhile. Our analysis reveals that high levels of share issuance significantly contributed to this underperformance. Prioritizing attractively valued, efficiently managed companies is crucial. To capitalize on current opportunities in emerging markets, investors should consider equity factors with a strong track record and the capability to navigate these markets’ unique challenges.

Attractive Valuations with Strong Earnings Expectations

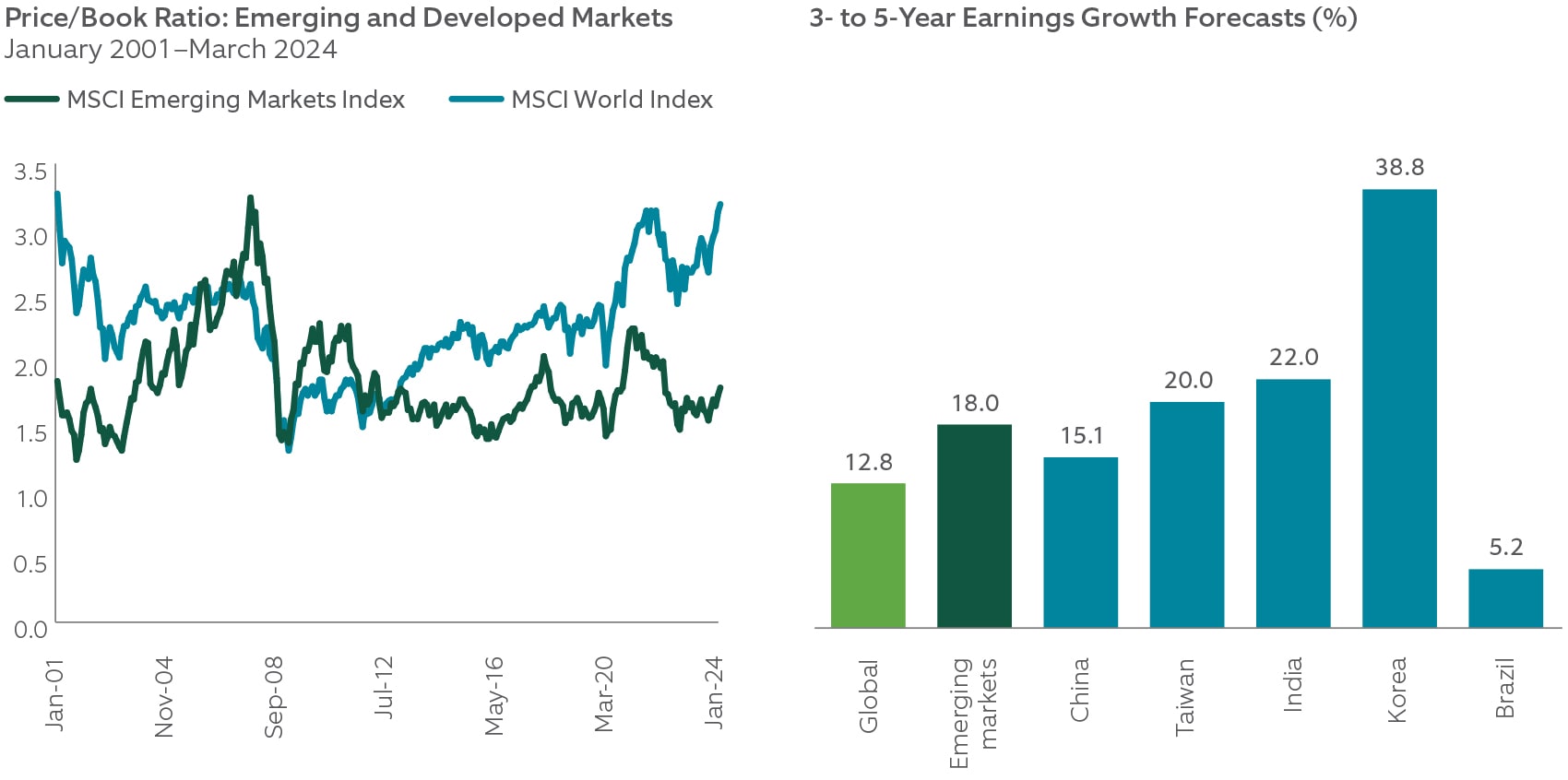

Emerging markets are trading at some of the most attractive valuations in recent history. As illustrated in the left panel of Exhibit 1 , the price-to-book ratio of the MSCI Emerging Markets Index is at a 40% discount versus developed markets (3.2 for developed markets versus 1.8 for emerging markets as of March 31, 2024), far steeper than the 20-year average discount of 17%. This valuation discount — often attributed to emerging markets’ price volatility, political instability and sensitivity to commodity prices — underscores inherent risks in these markets. However, we believe that these risks fall short of fully accounting for the valuation gap, suggesting that emerging markets are undervalued.

Valuations alone are not the sole reason to consider emerging markets. From a macroeconomic perspective, these markets continue to contribute substantially to the global economy and exhibit robust growth potential. Over the next three to five years, analysts project emerging market companies to achieve significantly higher earnings growth compared their developed markets peers, particularly in countries such as Taiwan, India and Korea. As shown in the right panel of Exhibit 1, analysts predict that corporate earnings growth in key emerging economies will exceed those of developed markets. We think this growth potential, combined with attractive valuations, makes emerging markets a compelling investment opportunity.

EXHIBIT 1: The emerging market opportunity

Emerging market equity valuations, as represented by the price-to-book ratio, are about 40% lower than that of developed markets (3.2 for developed markets versus 1.8 for emerging markets as of March 31, 2024), well over the historical average even as earnings growth appears attractive.

Sources: Northern Trust Quantitative Research, FactSet, MSCI. Returns are gross and in U.S. dollars. Data in the left chart is from January 31, 2001 to March 31, 2024. Data in the right chart as of March 31, 2024. Analysts’ earnings growth forecasts in the right panel are based on forecasts from First Call, I/B/E/S consensus and Reuters mean long-term earnings-per-share growth rate estimates. The three- to five-year forecasts are calculated using each individual broker’s methodology and provided by FactSet.

Share Issuance: An Emerging Market Malady

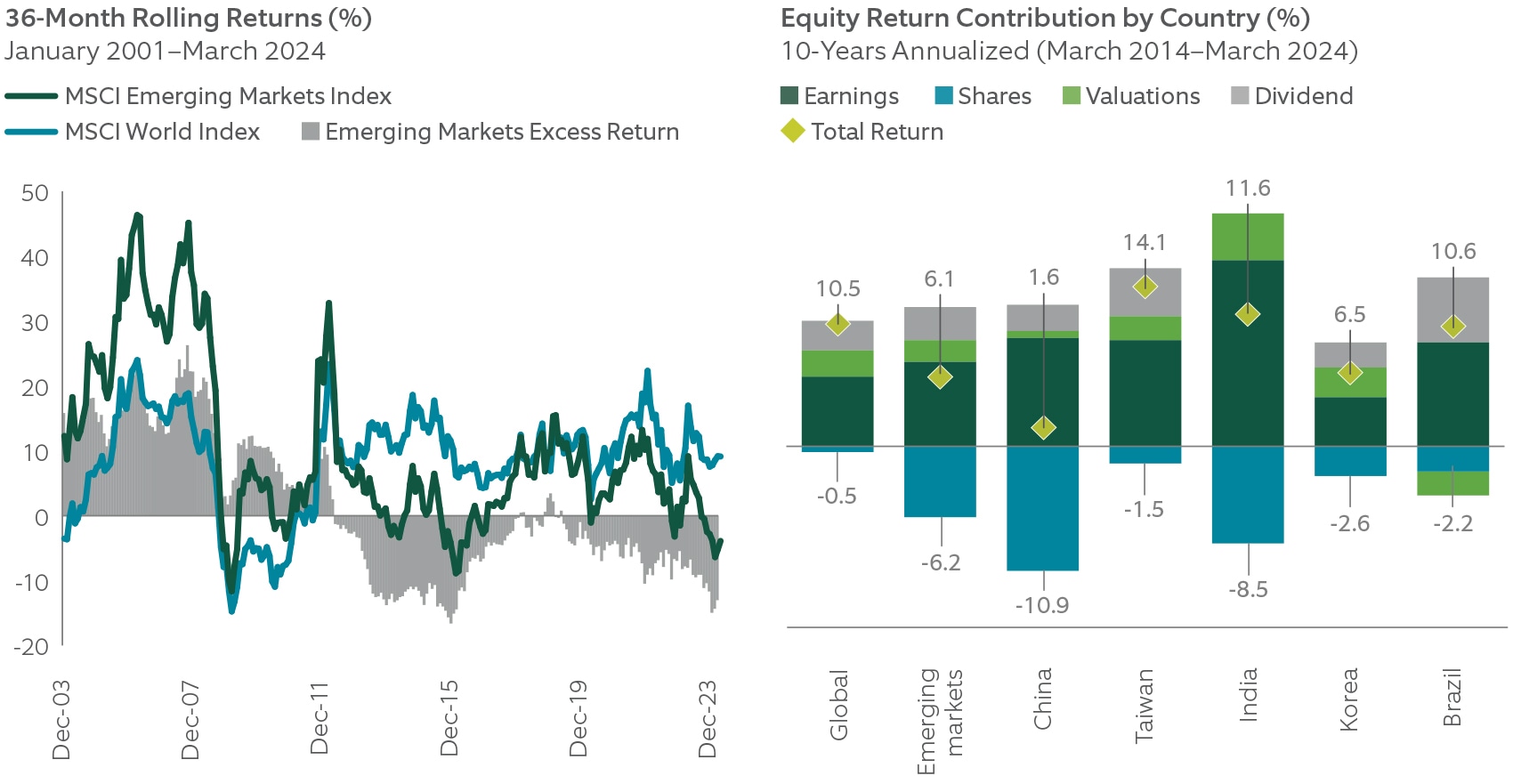

No matter the valuations, the prospects of higher returns in emerging markets have lured investors for decades. The MSCI Emerging Markets Index produced a robust annualized return of 8.3% from January 2001 to March 2024, outperforming the 7.1% annualized return of developed markets, as represented by the MSCI World Index.1 However, the last 10 years have proven a deep disappointment, as shown in the left panel of Exhibit 2 , prompting investors to reconsider their emerging markets allocations.

Our research shows that the disappointing results have largely stemmed from excessive share issuance by emerging market companies. While the contribution to returns from earnings growth in emerging markets over the last decade has been higher than in developed markets, a large volume of share issuance has consistently reduced earnings per share and lowered equity returns. Emerging markets companies have been issuing shares and diluting earnings primarily to raise capital for expansion, reduce debt and improve their balance sheets. Regulatory pressures and government policies encouraging debt reduction and financial stability further drive these companies to raise funds through share issuance.

The right panel of Exhibit 2 shows that share issuance reduced emerging markets returns by 6.2% compared to a 0.5% reduction for developed market returns. Consequently, share issuance dragged down the annualized return for emerging market equities to 6.1% from what would have been 12.3% gross of share changes. Over the same period, developed market equities maintained a return of 10.5% a year.

The right panel of Exhibit 2 highlights the return drag of share issuance in the largest five emerging market countries over the past 10 years. China’s substantial share issuance represents the highest dilution among emerging markets. Even moving forward, China is expected to continue issuing shares, albeit to a lesser extent, and many companies are even expected to increase their share repurchase activity. This emphasizes the need for investors to manage risks appropriately with emerging markets investments.

EXHIBIT 2: The Damage of share issuance in emerging markets

The issuance of new shares across emerging markets, especially over the past decade, lowered investor returns.

Sources: Northern Trust Quantitative Research, FactSet, MSCI, Bloomberg. Returns are gross and in U.S. dollars. Equity return contribution by country data is from 03/31/2014 to 03/31/2024. Index performance returns do not reflect any management fees, transaction costs or expenses. It is not possible to invest directly in any index. Past performance is not indicative of future results.

Factor Investing: Enhancing Opportunity, Mitigating Risks

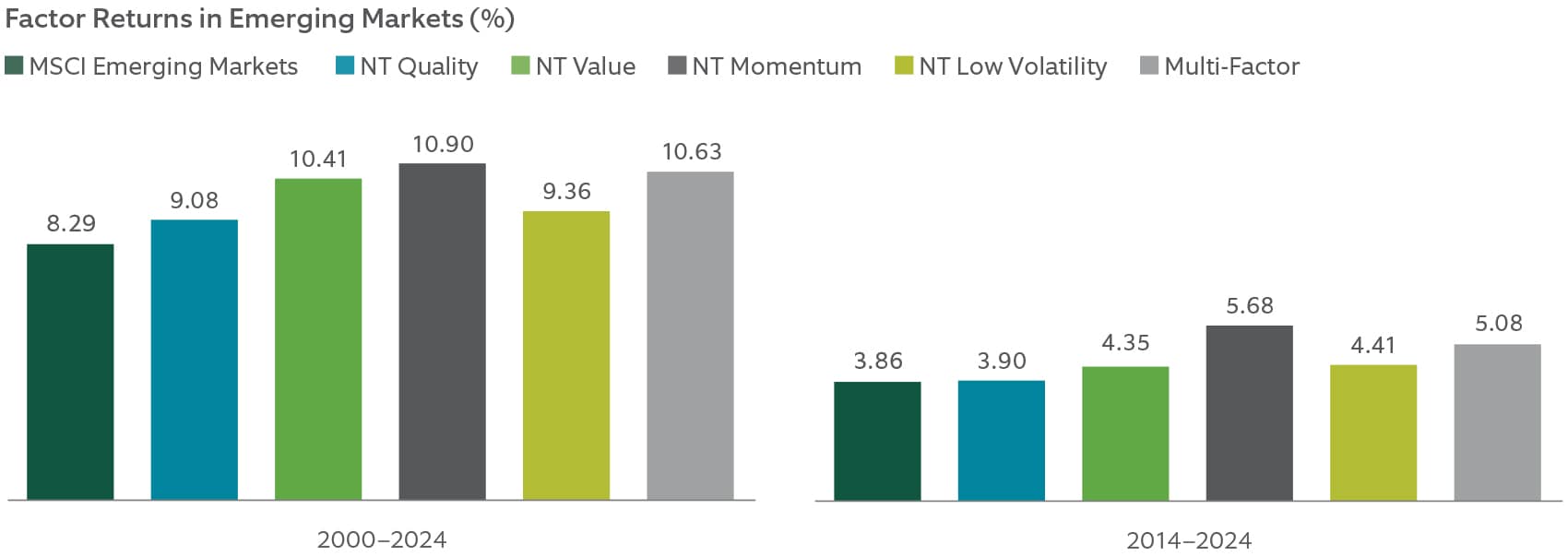

We believe that the resilient performance of style factors such as quality, value, momentum and low-volatility over time underscores the potential of factor investing as a powerful solution to capture alpha in emerging markets and to make the most out of the current opportunity. Style factors have historically delivered consistent sources of excess and risk-adjusted returns in emerging markets, paralleling trends seen in developed markets. Exhibit 3 shows that all factors, as well as a multi-factor portfolio that combines these factors, have delivered consistent outperformance versus the emerging markets index since 2000 and over the last decade.

EXHIBIT 3: The resilient performance of style factors

Style factors have historically delivered consistent excess and risk-adjusted returns in emerging markets.

Source: Northern Trust Quantitative Research. Returns are in U.S. dollar terms. Factor returns are simulated using Northern Trust factor definitions. Data is from December 31, 1999 to March 31, 2024. The multi-factor portfolio represent equal-weighted allocation to quality, value, momentum and low volatility factors. Past performance is no guarantee of future results. Index performance returns do not reflect any management fees, transaction costs or expenses. It is not possible to invest directly in any index.

In the previous section, we discussed how extensive share issuance in emerging markets has been a significant factor in explaining the low returns realized by investors. Our research indicates that these results also hold on a company level within emerging markets. In particular, companies that issue shares extensively tend to underperform companies that repurchase shares.

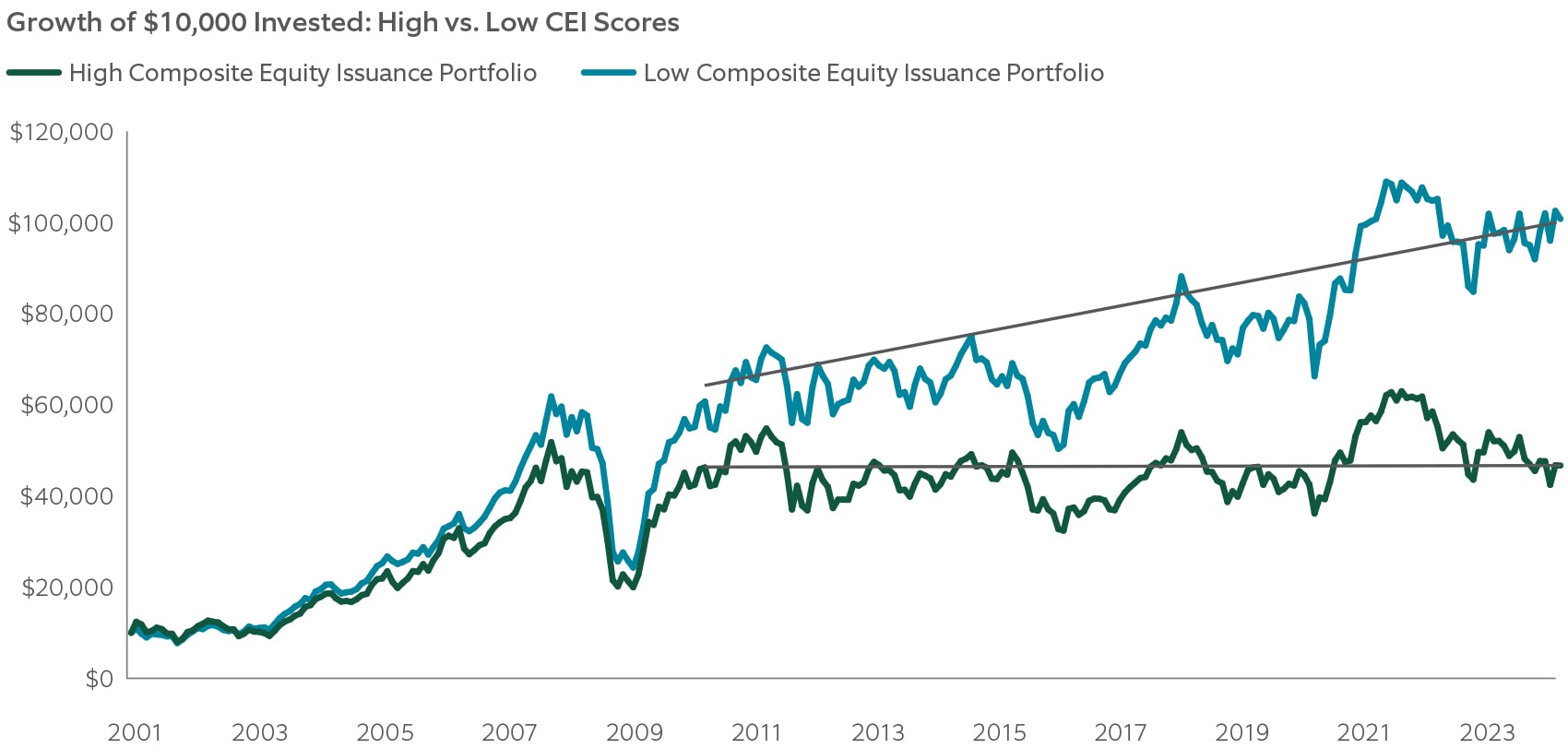

One way to address this dynamic at the stock level is to identify companies with more conservative approaches to capital management and consideration of total shareholder returns. Net share issuance (new issuance minus buybacks) is one approach that provides investors with good insight, but we prefer a more comprehensive measure that considers the full return to shareholders from capital activity. A measure that combines share issuance, repurchases and dividend payments is more strongly related to future stock returns. As part of our proprietary quality factor definition, we apply this comprehensive approach to create a composite equity issuance (CEI) score. A lower CEI score indicates better capital management and potentially higher future returns.

Exhibit 4 demonstrates the performance of two portfolios based on CEI from January 31, 2001 to March 31, 2024. A portfolio of stocks with the lowest 20% of CEI scores significantly outperformed a portfolio with the highest 20% of CEI scores. Notably, the high issuance portfolio has not shown growth for over 15 years. This finding emphasizes the importance of managing equity issuance risk in factor portfolio construction.

EXHIBIT 4: The positive impact of efficient capital management

Companies with high composite equity issuance (CEI) scores, which represents inefficient capital management, have not only underperformed companies with low composite equity issuance. They also have not generated returns for investors in more than 10 years.

Sources: Northern Trust Asset Management, MSCI, FactSet. Portfolios are monthly rebalanced, equally weighted highest and lowest quintiles based on composite equity issuance within the MSCI Emerging Markets Index. Returns are in U.S. dollar terms. All results are hypothetical and gross of any investment management fees. Sample period: January 31, 2001 to March 31, 2024.

Investors should exercise caution when constructing factor portfolios. Simple factor definitions and portfolio construction techniques can introduce significant unintended and uncompensated risks and leave unaddressed other risks, such as the increasingly important risk of return dilution. In emerging markets, where numerous extraneous risks are present, effectively managing multiple risk dimensions and exposures is crucial.

A Purposeful Approach to Emerging Markets

Despite recent underperformance relative to developed markets, emerging markets continue to offer compelling opportunities due to their strong outlook in corporate earnings growth and attractive valuations. Thoughtful and purposeful factor-based strategies can provide emerging markets investors with opportunities to improve their investment outcomes. These strategies not only have the potential to enhance returns but also address unique risks in emerging markets, such as earnings dilution.

1 Source: FactSet, returns in U.S. dollar terms from January 31, 2001 to March 31, 2024.