Post‑Pandemic Interest Rates: Lower for Longer

U.S. Treasury yields plunged to new all-time lows after the onset of the coronavirus pandemic, reflecting a flight toward safety by investors, the prospect of a very deep recession, and large-scale purchases of Treasuries by the Federal Reserve. How long-lasting will this environment of super-low interest rates be?

Some observers argue that once the pandemic passes, record-wide fiscal deficits, concerns about debt sustainability, and higher inflation will push nominal and real interest rates back up to, and potentially even above, pre-pandemic levels. Others believe that a combination of a larger private sector saving glut and implicit or explicit nominal yield curve control by central banks will keep interest rates low long after the pandemic has passed.

History offers evidence for even-lower-for-longer outlook

Both sides make good arguments, but only one can eventually be right. As already indicated in our recent Cyclical Outlook, “From Hurting to Healing,” we believe that we have entered a “New Neutral 2.0” environment of even lower interest rates for longer. The history of pandemics and interest rates over the past seven centuries; of U.S. policy, inflation, and interest rates in the post-war 1945–1951 episode; and the experience following past recessions all provide evidence supporting this thesis.

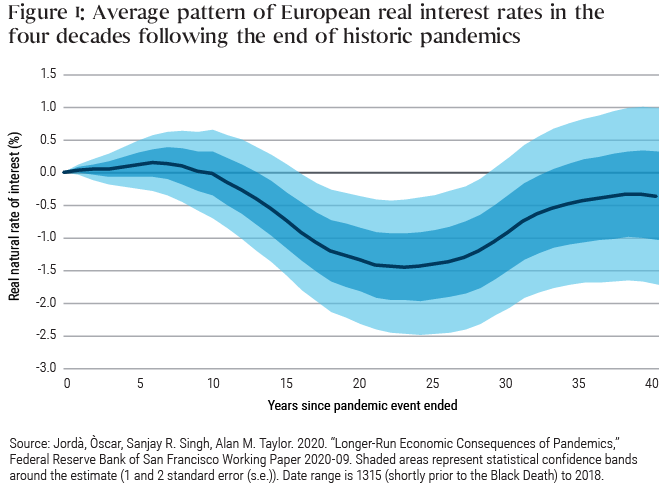

Starting with the history of pandemics, in a recent working paper published by the San Francisco Federal Reserve Bank, Òscar Jordà, Sanjay Singh, and former PIMCO senior advisor Alan Taylor studied the path of real interest rates following 15 major pandemics since the 14th century that each cost more than 100,000 lives. The authors conclude that these pandemics had long-lasting economic effects, lowering the real rate of interest for decades after the end of each pandemic (see Figure 1, drawn from their paper).

The authors speculate that the decline in the rate of return reflected depressed investment opportunities due to excess capital per unit of surviving labor and/or a heightened desire to save due to increased precautionary saving or a rebuilding of depleted wealth. They also show that their results are robust to possible major trend breaks and to the exclusion of the two most extreme events in their data set, the Black Death (1347–1352, approximately 75 million deceased) and the Spanish flu (1918–1920, approximately 100 million deceased).

Of course, this time may be different. There are two main caveats. First, as the authors themselves point out, prior pandemics significantly decimated the labor force and therefore created a scarcity of labor relative to capital that may explain some of the decline in the return on capital in the historical data. By contrast, the majority of victims of COVID-19 have been older individuals, who make up a smaller proportion of the labor force. Thus, based on the evidence so far, it seems unlikely that the labor force trends will be as significantly affected by COVID-19, and the impact on the real interest rate may therefore be smaller than after past pandemics.

The second difference to earlier pandemics is the size of the fiscal response, which this time around is very large: Many major governments are looking to fill the hole in incomes and aggregate demand created by lockdowns and social distancing. Higher fiscal deficits and debt levels could cause concerns about fiscal sustainability and, if fiscal policy stays expansionary after the pandemic is over, may also lead to higher inflation. This could then push real and nominal interest rates significantly higher, or so the story goes.

Long-term net impact of COVID-19 on interest rates

Despite the above caveats, the net impact of the coronavirus pandemic on interest rates is likely to be negative in the foreseeable future, for two reasons.

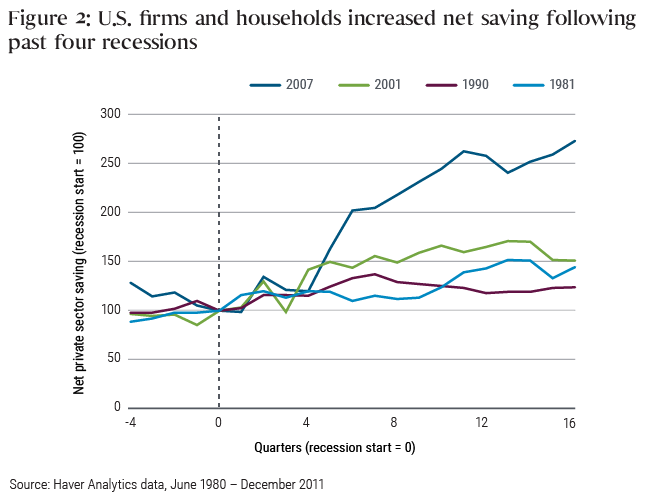

First, while the public sector is dissaving (i.e., running larger fiscal deficits), the private sector – both individuals and firms – is likely to want to save more for years to come. As Figure 2 illustrates, this also happened after the previous four recessions, with the response particularly large after the global financial crisis (2008–2009). Following this current recession, we expect households will want to rebuild lost wealth and increase precautionary saving, particularly in the form of liquid assets such as cash and bonds, but also in the form of higher home equity (and thus lower mortgage debt). Also, firms will likely strive to increase cash on the balance sheet and reduce net leverage. Thus, increased private sector saving should provide a powerful offset to higher public sector deficits.

Second, in an effort to ensure that higher government debt doesn’t push bond yields significantly higher, central banks will likely keep short-term interest rates low and cap intermediate and longer-term bond yields via large-scale purchases and/or more direct forms of yield curve control. With debt-to-GDP ratios expected to be significantly higher after the pandemic passes, monetary policy will likely have an important role to play in helping governments cope with the debt in ways other than outright default or recessionary austerity.

There is a precedent in modern history for how this can be done: Following World War II, the Fed kept in place a lid on long-term Treasury yields (at 2.5%) that had been originally implemented when the U.S. joined the war. Thus the Fed helped keep government borrowing costs low during the post-war economic boom and high inflation. With nominal GDP significantly exceeding the nominal interest rate on the public debt, the debt-to-GDP ratio deflated without harmful consequences for the real economy.

Only when inflation exceeded 20% in the early 1950s did the Fed resist a further monetization of government debt, and the Fed finally gained independence in setting monetary policy with the Treasury-Fed Accord of 1951. Interestingly, the New York Fed’s Liberty Street Economics blog recently published a historical account of how the Fed managed the yield curve in the 1940s . It’s doubtful the timing is a mere coincidence.

In summary, while the health and humanitarian crisis of COVID-19 will eventually pass, and hopefully sooner than later, the depressing effects on interest rates will likely linger for a long time. Investors should brace themselves for a New Neutral 2.0 world of even lower real interest rates for longer.

This blog post was published on 13 April 2020.

Read PIMCO’s latest Cyclical Outlook, “ From Hurting to Healing ,” for detailed insights into the 2020 outlook for the global economy along with takeaways for investors.

Please see PIMCO’s “Investing in Uncertain Markets” page for our latest insights into market volatility and the implications for the economy and investors.

Joachim Fels is PIMCO’s global economic advisor and a regular contributor to the PIMCO Blog.

All investments contain risk and may lose value. This material is intended for informational purposes only. Forecasts, estimates and certain information contained herein are based upon proprietary research and should not be considered as investment advice or a recommendation of any particular security, strategy or investment product. No part of this material may be reproduced in any form, or referred to in any other publication, without express written permission. PIMCO is a trademark of Allianz Asset Management of America L.P. in the United States and throughout the world. THE NEW NEUTRAL is a trademark of Pacific Investment Management Company LLC in the United States and throughout the world. ©2020, PIMCO

RSS Import: Original Source