Kandi Technologies (KNDI): With a 12 month $17 Share Target -A Conundrum For Longs And Shorts Alike

Abstract: After some 43 years top level business experience, all in the equity financial sector, along with nine as a KNDI shareholder, I know how to do detailed Due Diligence on public companies. In all my professional years, I have never experienced a public company accomplish so much, starting with so little against such incomprehensible odds be so maliciously maligned with erroneous information as China based PEV leader, Nasdaq listed Kandi Technologies. The Conundrum for Shorts is KNDI’s exceptional growth now on the cusp of hyper-growth, while being stuck in a 5.5 million (18% of float) short position with daily volume drying to 200,000, share borrowing cost over 20% and few additional defensive shares to borrow. This while having all but one misconceived minor concern after years of attack issues now de-bunked and that one will be gone in 30 days or less. The Conundrum for Longs is whether to buy now, with the stock back to 2008 prices, or wait and shortly chase it higher. The case for this inevitable upside outcome and $17 12 month target is in this report.

Authors Note: Due to the length of this article, I have chosen to put this out prior to the weekend so all shareholders and interested parties will hopefully have time to read it in its entirety.

Summary Past Four Weeks

- August 22, KNDI announced new 5th Pure EV (PEV) model, the very hi-tech K21 targeting China’s massive Ride-Hailing Market Led by Didi Chuxing. Production expected to beginning Early 2017 with first year sales in excess of 30,000 EVs.

- August 8, KNDI announced $45 million new EV development grant with $15 million advanced from Hainan Provincial Government the Location of its 4th new 100,000 capacity Manufacturing facility that will produce the K21.

- August 4, 2016 KNDI’s K17A, a new Hi-tech version of China’s 2015 PEV of the Year Award Winner, co-developed with Alibaba & ZTE technology released for sale initially in Shanghai. Local Media expects KNDI sales to top 35,000 units in 2016.

- Geely Holdings, Sole Owner of Volvo, London Black Cab & 43% of Geely Auto acquires Geely Auto’s 50% of KNDI JV Opening path to JV receiving its own manufacturing license and subsequent IPO.

- Q2, 2016 KNDI Resumes its PEV leadership position with 7400 units sold, expect 35,000 Full Yr. 2016 EPS up 40% to $.85

- July 24, KNDI announced 60,000 (Approx. $1.2 billion) Multi-Year Purchase Agreement for New Government sponsored College CarShare Program with China’s Largest Auto dealer Pang Da with 1250 locations. From CC, Pang Da will now also represent for consumer sales of all KNDI’s 5 current EV models.

- In just the past 24 months KNDI JV has sold some 40,000 PEVs, with over 30,000 now in the World’s largest CarShare program.

- Above revelations and KNDI’s 5.5 million share short position recently reported with 21 Days to Cover, 18% of float and 20+% share loan rate likely cause of recent short attack article published wrought with erroneous information to be exposed.

A Short’s Conundrum Possible Accelerator- As you can see from the above Summary, it has been an incredibly positive four weeks for KNDI’s business, however the stock has declined 10%. Why? Simply stated, short-sellers concerned about KNDI’s recent fundamental revelations paired with fear of its perennial year end quick double are doing whatever it takes to constrain the stock. This done by attacking all good reported news and even have gone so far as to publish an article based only on fictional problems irrespective of the facts, all to be addressed below. But note on the chart below. In each of the past five years, KNDI has seen its stock sprint to at least a double off a low in H2 in 60 days or less. The major difference this year than in the past is KNDI has entered the second half in its strongest fundamental position ever. This even before its JV receives the first $110+ million tranche of an already earned $160 million+ China National subsidy check expected in the next few weeks. But more on this later.

Wrought with confusion created by KNDI detractors, perhaps it is a good time to give a short refresher on KNDI’s short eight year evolution from a non-descript Recreational Off-road Vehicle maker, to China’s top independent PEV maker.

What actually is KNDI? An EV Parts Supplier or EV Automaker?

KNDI is both and here in lies the confusion and makes good fodder for those detractors and short-sellers who have an agenda against the Company. A confusion initially caused by China’s ten year ban on issuing new Auto Maker licenses begun in 2006. At that time, a moratorium was put in place to stop the rampant growth of Internal Combustion (ICE) passenger car-makers. With over 150 licensed, it was becoming too burdensome for regulators to keep track. So to encourage consolidation, all new license issuances were halted. KNDI which first began trading in the US in 2007, was in its infancy as a quite successful off-road recreational vehicle (ORR) maker, (ATV, UTV, Go Carts, Dune Buggies etc.) regrettably did not have a passenger car manufacturing license. However, by 2008, KNDI’s ORR export business was doing well manufacturing close over 40,000 ORR vehicles annually . So there is no question, KNDI knows how to manufacture and sell vehicles.

In 2009, KNDI introduced its first Electric Car, a small Low Speed Electric Vehicle (LSEV) the CoCo for export (if you look close on this page you will see a pic of me driving one). Several thousand CoCos were sold in the US. In late 2009, KNDI made a slightly larger two seat EV with lead acid battery called the KD5010 which through a loop-hole in the license moratorium, allowing it to be registered as a “truck” further allowing it to be produced and sold in China. Initially a thousand were sold early 2010 in China; mainly in its home city of Jinhua . In late 2010 it switched to lithium batteries and expanded to Hangzhou China where due to its patented unique way of quick changing the battery through the cars “rocker panels ”, started selling these little “trucks” in 2011, each with the ability to change the battery in two minutes. After a year and several thousand sold, lobbying by licensed EV Manufacturers caused the “truck” loophole to be closed by the government, temporarily halting KNDI’s ability to sell the EVs in China.

So this is when and where KNDI Chairman Hu again showed his nimbleness. He quickly signed an agreement with one of China’s second tier international automakers, Zotye in 2012, which allowed KNDI to still manufacture 99% of the complete EV, but with the last 1% and license provided by Zotye. The agreement with Zotye was simple and similar to KNDI paying Zotye a licensing fee which equated to less than $100 a car. This structure allowed KNDI to book all revenues on its own financials. Next comes the KNDI, Geely Auto (GA) JV.

In mid-2013, KNDI and GA (00175.HK ) announced an LOI for a 50-50 JV . At that time, KNDI, on its own “nickel” was near completing the ground up construction of the first ever “build from scratch” PEV 100,000 annual capacity plant in Changxing China . At closing of the JV in late 2013, both KNDI and GA contributed $80 million USD in cash to the JV. Simultaneously, KNDI sold the Changxing facility to the JV and GA also sold an equal value 100,000 capacity plant to the JV. At closing, it was agreed that KNDI and its Chairman, Hu Xiaoming, would manage all plant operations and KNDI independently and additionally would make and sell parts such as the Electric Motor, AC, Controller, etc. Additionally, since KNDI did have a Battery Maker license, as in the case of TSLA, KNDI would also assemble and sell completed Battery Management Systems (BMS) to the JV. GA would effectively be the silent partner but contribute the use of its Manufacturers license in perpetuity and sell some body parts from related EVs like the Panda and K17 to the JV. However, since both companies were public, and the JV was 50-50, both agreed that neither would be allowed to “consolidate” any of the JV numbers in their respective reported audited financial statements except under the equity method which requires the showing of profits or losses at the bottom line.

After the JV went into full affect in early 2014, KNDI’s Gross 25% Margin (GM) declined substantially due all EVs to be made in the JV. This caused by KNDI not being able to show its half of the JV revenue numbers, only the revenues of parts and batteries sold to the JV. It is because of this “Equity” method of accounting not allowing any of the JV revenue numbers to be shown by KNDI, that has created the current confusing environment giving a window to KNDI short sellers, detractors as well as computer generated websites to accuse the Company of low revenues and margins relative to industry standards. For example; if KNDI had been allowed to consolidate its half of the JV revenues in Q2, its top line revenues would have been approximately $112 million instead of $55 million . Not likely that KNDI would be trading with only a $300 million market cap, if it was showing consolidated top line revenue numbers of $112 million in the quarter . KNDI’s own GM as a parts supplier for now only to the JV is below industry average because it must be the lowest “bid” to maintain the business. However it makes up the difference in the all-important bottom line when half of JV bottom line is added. There is no restriction against KNDI selling parts outside the JV, but according to Hu on a recent CC, that will come later.

In late 2015, the China government opened up a new special category for EV Maker licenses. The JV immediately applied to get its own license. However, after an initially unexplained delay, not just to the KNDI JV, but all EV makers who applied. Do to such a high demand for these new licenses, in late Q2 16 the Government again changed the rules before even issuing any new licenses. Under the new rules no new license would be given to any prospective EV maker whose share structure includes a major shareholder who already has an auto manufacturing license, i.e. Geely Auto. Obviously, such a last minute change was likely forced by lobbying efforts of major ICE car-makers trying to quell upstart EV competition. Since KNDI and the JV had already publically announced more than a year ago that the JV was preparing for a China listed IPO , common sense would dictate that the JV should have its own license by the time of the IPO. So with the JV Company in a stalemate due to GA’s pre-existing license, the only way to unlock, would be to have GA dispose of its interest. Since GA Chairman, Li Shufu knew that KNDI’s smaller EV’s, particularly in a CarShare or Ride-hail environment, should have a bright future, the jointly agreed upon solution was to have his personal 100% family owned Holding Company, Geely Holdings (GH) buy the interest from GA. For those who are not aware, GH, NOT the pubic GA owns 100% of Volvo and London Black Cab stock along with a myriad of other private companies. The only relationship GA has with Volvo is a Technology Sharing agreement. GH also owns 43% of GA shares.

It is because of this stalemate that Geely Holdings and KNDI felt it was in the best interest of all parties, including GA, for GH to buy the GA KNDI JV interest. Since, for good reason as explained later, the KNDI JV had its first quarterly loss in Q1 16, it made it easier for GH to “get the votes” to complete the deal. Did he under pay for the 50%? Perhaps, but what good is it to GA the behemoth, public company to be “stuck” in a Private 50-50 JV where they could not show anything but bottom line on their own books and would never be able to bring public? So what did GH really pay? Well 30 months ago, as mentioned above, both GA and KNDI each paid $80 million. At recent purchase, GH paid GA $111 million, plus assumed $67 million in loans and guarantees owed GA by the JV. So GH paid in cash and risk effectively a double what GA invested the JV just 30 months ago. Arguably a more than fair price if one were to believe short-seller and detractor claims that this was a “JV gone bad”. From a KNDI and JV Management point of view, the ability to have to only deal with one person, Li Shufu, rather than a whole chain of GA Management at each step of JV development and expansion is obviously well received as commented by KNDI Chairman Hu on the Companies recent Conference Call . More on this later.

Recent Developments

The New K21Built For Ride-Hailing

Mondays Press Release on the new K21 was quite the surprise in both new EV and scope, but perhaps not totally unexpected. Over the past two investor conference calls, while discussing KNDI’s new 100,000 annual capacity Haiku, Hainan Province manufacturing facility, when asked “what EV will be made in Haikou”, Hu would only say; “for now let’s keep it a surprise. It will be an EV that all will be excited about”. Putting more “tea leafs” together, from recent 10K & 10Q filings and China Media articles, though never released in a PR, it was divulged that KNDI and UBER were working together developing an UBER driver lease program, initially with 200 K17’s. On the CC, when asked how the program was going, Hu responded, it is going well, but not quite ready to say any more right now, other than UBER was not the only Ride-Hailing program KNDI is working with . Since UBER China has around 10% of the China Market and Didi Chuxing with 87% of the market, the two were effectively the whole market in China. As reported a few weeks ago UBER agreed to be bought by Didi Chuxing, who though only in China at this time, is thought to be bigger than UBER worldwide. The pieces of the puzzle have now come together with the reading of Hu’s PR quote in the PR. In the image capture of the PR below, the “boldface” is mine pointing out important areas. None more important that forecast to produce in excess of 30,000 units in 2016. As witnessed by actual KNDI performance beating reported total unit sales Guidance by 20% on each of its last two “guided” periods, if 2017 sale of the K21 alone only reach 30,000, this will add approximately $700 million to JV 2017 revenues. With the K21, it will bring KNDI developed EVs up to five with three new this year alone.

While KNDI detractors continuously make light of KNDI and its stable of EVs, it is noteworthy that each of the three new EV’s released this year have been spawned under a “ Technology Sharing Agreement ” originated by KNDI CEO Hu and signed by Alibaba, ZTE, Geely, UBER, Minsheng Bank and others last year. If you note the K21 featured technology in the above PR, you will see that it is but a few steps away from being self-driving. (Appropriate side note: Volvo is considered one of the most advanced developers of autonomous self-driving vehicles. Not coincidental that UBER’s first “self-driving” car to be introduced in Pittsburg in the next few weeks is a Volvo .)

$45 Million Hainan Government Grant for new EV Model

This is a very meaningful announcement that should logically squelch any reasonable doubt about KNDI’s legitimacy, staying power and stellar reputation in China’s EV Industry. While maybe not clear to the less knowledgeable KNDI investor, this R&D subsidy payment is being made Directly to KNDI , not the KNDI JV . While adding to the mystery addressed above about “what EV is going to be built in the Haikou, Hainan Province facility”, with this release the question was answered with unveiling the K21 above. To expand on Haikou; the new KNDI $300 million, 100,000 EV facility under construction is becoming somewhat of a “marvel” in rapid plant construction lore in China. The agreement to build this facility was signed Dec. 13, 2015, Ground Breaking , Jan. 28, 2016, topped out this month , and expected to be completed this year with K21 production beginning in early 2017.

Of particular note, this plant is being built and funded by KNDI at this “break-neck” pace through Government supported, low interest bank loans, not the JV or any need for equity funding. Quite amazing when one considers this one plant alone will cost more than KNDI’s total depressed market current market cap . The reason the plant and $45 million new EV R&D grant was contracted through KNDI rather than the JV, ties to Chairman Hu’s strong, long time relationship with the Hainan Government. Now a logical investor must ask himself; “If KNDI is in such ‘dire’ financial condition as detractors are trying to make out, why are the Haikou and Hainan Governments so willing to work with and pay money to KNDI directly AND, why is KNDI in such a hurry to finish this plant? ” I might also add, that KNDI alone has already paid $54,448,198 ( Q2 16 10Q pg. 23 ) of its own funds toward this construction. This makes up right at half of its total Accounts Payable, since it came from bank financing. Upon completion, it has already been contracted that the JV will buy the facility from KNDI.

Here is the PR put out by KNDI two weeks ago:

The New Gen K17A

A mentioned in the “bullet” above, this is the new higher speed, higher range hi-tech version of the KNDI K17 which was awarded the 2015 Pure Electric Passenger Vehicle of the Year this past January.

As mentioned above, this new-gen K17A is faster and with extended range compared to the Award Winning K17. If you read the full PR on the K17A below, you will note that this EV also has added a larger “touch-screen” has full wireless Internet access as well as 3G Cell access and many other hi-tech features. But most importantly, after subsidies and other discounts, the K17A went on sale for the first time in Shanghai on August 4th with a cost to consumer of 78,000rmb or only around $12,000 dollars . An amazing price particularly when you consider that Shanghai, due to over saturation of all types of vehicles has an auction process that requires anyone wanting to buy an ICE car bid for a “permit” to apply for a license. This confirmed as quoted here from this recent June Forbes article “… getting a plate for a petrol-powered car can cost up to $12,000 in a city like Shanghai ”. So, a Shanghai permit alone, even excluding the 10% additional sales tax an ICE buyer must pay, cost about what a Shanghai resident would pay to own a K17A outright . From this recent China media article , you can see that K17A sales expectations by China media are high this year, not only for the K17A, which Hu already stated in the YE CC that he expected K17A sales this year alone to be in the 20,000 area, but all KNDI EVs. (IMO, while author’s titled 50,000 looks somewhat high Re. sales this year, the whole translated article is a worthy read with pics)

Q2 16 Unit Sales & Financial Results Plus $17 Share target Calculation

Once again, KNDI prior sales Guidance was soundly beaten on the upside in Q2. At Q1, guidance was given for sales of 5500-6000 in Q2. As you can see from the PR below , in July a guidance increase alert was published by the company raising expectations by 10%. As was the case in a similar guidance raise alert in January for full year numbers, KNDI actually beat Q2 top Guidance by 20% reporting actual JV sales of 7,200 as can be seen from the 2nd PR below.

As it turns out as you can see form the China media article below, a pleasant surprise in that KNDI once again, rose to the top of all China PEV makers in the month of June with 4670 units sold. This is the fifth time KNDI has achieved that top monthly honor in the past twelve months.

Why was this a pleasant surprise? Well a lot happened in the EV Industry in China since KNDI had its last top position in December. A “happening” that caused KNDI to have no sales at all in Q1! Let me segue here to explain.

As reported by the Company on its 2015 YE Conference Call in March, the PRC Government, once again in a surprising announcement, “changed the EV rules” in December 2015 for 2016. It raised both the minimum speed and range requirements to receive subsidies and 10% sales tax abatement. Prior to the unexpected change, all A00 category EVs (City EVs) were only required to have a top speed of 80kmph and range of 120km. This made sense since the top speed limit in any China city is 80kmph, additionally, the 120km range, would last the average City driver a week on a single charge. Since all of KNDI’s EV are specifically designed for city use, it made no prior sense for the Company to arbitrarily add to the cost and weight of the EV by going for a higher speed and range if not necessary. This change affected all A00 category makers or around 16 manufacturers.

However, this last minute surprise once again shows the brilliant flexibility of KNDI’s Chairman/CEO Hu. He made the immediate decision to halt all JV sales and production in January and began upgrading all four KNDI EV’s (K10,K11,K12,K17) to meet the new 100kmph and 150km range requirements. He also “took the hit” and recalled all unsold EVs from dealers which were also upgraded. It wasn’t just a matter of “upgrading and back on the market”; it also required upon completion a Government required recertification. Amazingly, KNDI made all the upgrades and received recertification on all its EV’s by the first week in April. So contrary to what short-sellers and detractors might “spin”, the JV’s lack of any sales in Q1 was caused by this alone. Not any KNDI specific problem.

What is most amazing is that in spite of having no sales in Q1, quick R&D and retrofitting cost on all four labels, along with maintaining three completed 100,000 capacity facilities, the JV ONLY lost around $9.5 million in Q1. Half of which KNDI had to book as loss to its own bottom line. Yet, KNDI itself still managed to eke out a small GAAP and $.07 Non-GAAP profit in Q1 from selling parts to the JV for Q2 production resumption. So to see KNDI so quickly back at the “top of the heap” so quickly was a pleasant surprise.

Let’s look at the Q2 highlights as reported by the Company .

Now remember, the revenues reported here other than net income are KNDI’s alone from parts and battery sales. Had half of the JV sales also been added, Q2 revenues would have more than doubled to $112 million as mentioned above. Note that significant difference between GAAP and Non-GAAP in the Company “bullets” above, both in Q2 and last year. The Main contributor to the difference was the non-cash charge that had to do with employee stock and stock option awards. Of these, very little went to Management on the stock award side, though higher on the stock option side. Though not easy for them to sell, Chinese employees like the thought of owning US stock. The non-cash charge under GAAP accounting for Q2 options alone was -$8.7 million or around -$.19 a share. (For the 1st half around -$.35). Yes, it makes a dramatic difference in the current “PE” reported since most financial services websites report GAAP only. Now these options have an exercise price of $9.76 a share. In other words, if and when they are exercised, the holder will have to pay $9.76 per share in cash to the Company. At anything around the current price, not exactly a “bargain”. So for short-sellers and detractors being “outraged” (though I never could understand why they would be outraged if they were short) and accuse Management and Employees of “stealing” from the Company by these awards is a bit “over-the-top”.

Let me remind. This stock & options award plan was voted on and approved by a majority of “outside” shareholders only in 2013 and went into effect in 2014. This was the first opportunity the Company had to offer stock incentives since 2009. Salaries in China are but a small fraction of what they are in the US. Hu’s annual cash salary only recently passed $30,000 a year. Additionally, Hu has been personally guaranteeing some $25-30 million a year of KNDI bank debt for the benefit of all shareholders in order to achieve a lower borrowing cost. He has done this since the Company has been public. So yes, it would have been nice for KNDI to have recorded GAAP income of close to $.30 a share in H1 earnings were it not for the stock awards non-cash charge. This particularly when one considers this level would have been reached with sales of only 7200 units in Q2. Just imagine what it would be in a year when quarter sales start tripling. But I believe an intelligent investor should look at it as a relatively “fixed” charge that will stay effectively the same and become less noticeable as EV sales continue to dramatically ramp up due to all of the “Goodwill” spread by distributing these awards to employees.

Should KNDI reach the 35,000 unit sales for full year 2016, which is not unrealistic since the JV sold a total of 24,100 in 2015 after selling only 6,002 in H1 2015; when considering the EVs being sold this year are all new and higher priced, KNDI should easily beat the Non-GAAP $.61 EPS 2015 , by $.25 and come in over .86 per share for 2016. Furthermore, based on existing contracts, along with no more surprises from the China Government, KNDI should sell at least 70,000 EVs in 2017. At this level, EPS should project between $1.50 and $1.90 for the full year. Calculating at 20 times multiple of this year and 10 times mid-range next year’s earnings is what I base my $17 target price for 12 months out.

Last point from the financial “bullets” above and an observation. Look at KNDI’s positive Working Capital Surplus of $67.4 million, or about 25% of its current Market Cap. With all you now know about the Company, does this look like numbers from a Company in trouble as short sellers claim? While not in the bullets, the long standing mantra from shorts and detractors of “way too high cash burn” is getting stale. Wednesday on CNBC, NYU Stern Business School Professor, Aswath Damodarn said it best; “To accuse a fast growing young growth company of burning cash is like accusing your elementary school child of not acting like and adult”. KNDI is a leader in a future Trillion Dollar Industry. If you want it to stay a leader, expect it to burn cash. What Hu has accomplished while only raising around $140 million in total equity since going public is nothing short of amazing. Particularly, when China’s subsidy payments to the JV, now totaling over $160 million, with $110+ million expected in the next few weeks have taken so long to be paid. Yes, it is this eminent nine digit subsidy payment which is the detractors and short-sellers last “open item” held against the Company. Continuously, for the past few months, this issue has been pandered all over the Internet as “sure sign” that KNDI must be “in trouble with the China government”. But while it may have been effective in shaking out some innocent shareholders, the facts show differently.

Just what are the “facts” of the Subsidy hold-up?

The fact is that no China EV maker has received any National Subsidy payment for any sales made after H1, 2015 as can be gleaned from the recent China Article this quote comes from; “ As state subsidies last year and the first half of this year so far have not led to car companies issued cash flow is very tight…” No EV maker has received any subsidies for H2 15 sales or the now also due, H1 16 sales. In KNDI’s case the combined payment will be for approximately 25,000 EV’s already sold. While in its infancy, the Subsidy payment schedules have been erratic. Since inception of the National Subsidy program, KNDI JV has received three checks totaling $135.7 million for 17,051 EVs for all sales though Q2, 2015. The next check expected in the next few weeks will be for 18,104 EVs sold in H2 15 and should be in the $110-120 million range. Since the subsidy program called for an annual sliding scale down when first formulated in 2013 (-10% 2014, -10% 2015, -10% 2016, -20% 2017, -20% 2018, -40% 2019, -40% 2020 >, Subsides End.) Not some new “punishment” that detractors claim, KNDI’s Q1 2016 subsidy payment will be 20% less per EV then its H1 2016 Payment for 7200 EVs already sold, or $40 to 45 million. Assuming things go back on schedule, the second payment should be received in November. A last noteworthy point. This sliding scale that has been in effect for several year now is the reason Q4 always has so many more sales. Consumers and businesses alike want to capture the higher subsidy. In the past, it has only been 10% per year, now that the drop will be larger, expect an even more explosive Q4. Not just for KNDI, but for all China EV sales.

This “back-slope” reduction while always anticipated, is not nearly as bad as it might seem, as beginning in 2017, it will be supplemented with the start of Carbon Credits trading formulated after the California model. A model that TSLA has milked for almost $750 million dollars since in the EV business. KNDI will be positioned particularly well when it is started in that both KNDI as an EV parts maker and supplier and the JV will both be ranked carbon negative and each will have credits to sell. Additionally, since each of KNDI’s four facilities are I different Provinces, and the trading will initially be rolled out Province by Province, KNDI will have a robust and growing market to sell its credits. Furthermore, because KNDI’s four new 100,000 capacity facilities were built specifically for EVs with state-of-the-art assembly lines, it will always be able to compete as long as the “playing field” is level, with or without subsidies or even credits.

In the recent short-seller attack article I have been alluding to; a false claim was made that the hold-up on KNDI’s subsidies was KNDI specific as a pre-cursor of penalties about to be levied on KNDI because of mis-use of subsidies. While that makes for a good story to scare unknowing investors out of the stock, it could not be further from the truth as you now know. That writer also claimed that the reason KNDI JV halted production in Q1 was because the Government “shut KNDI down” for this same reason. You now also know this latter accusation was false so let’s quash this as well.

The only viable portion of his KNDI allegation is that there has been an ongoing investigation of ALL 90 of last year’s subsidy participants. Yes, since ALL participants were being audited, KNDI as EV leader was one that would naturally draw the attention of reporters, just like BYD who supposedly even had a mid-level executive commit suicide over guilt of cheating on the subsidy for BYD. In KNDI’s Q1 CC, Chairman Hu brought the whole investigation to the forefront in his opening comments in giving a “heads up” that subsidies might be delayed for everyone because of the investigation of ALL participants. However, Hu made it quite clear that KNDI welcomed the investigation to cull out cheaters and shared the “investigation team’s” positive comments on KNDI JV and its business model. This from the Q1 16 CC:

And in an article published from China National Cable TV , some ten “supposed” violators were named, to include some much larger Companies than KNDI. Needless to say, KNDI was not included. But if the payment delay has you concerned about whether KNDI and the JV can handle its debt, remember, Hu and Geely Holdings Li Shufu have a combined net worth a dozen times higher than KNDI and the JV combined. GH Li has an ego even bigger than KNDI’s Hu. Look at what Li has accomplished with Volvo: After buying Volvo from Ford in 2011, he subsequently put in almost $10 billion US more . For the first time in the 89 years Volvo has been around, it passed a half million cars in 2015 with large profits. On top of that, Li is as passionate for EV’s as Hu is as can be seen by this article .

KNDI signs 4 Yr Government Sponsored 60,000 ($1 Billion+) Deal with Pang Da, China’s largest Auto Dealer with 1250 locations.

Another blockbuster PR by KNDI and the stock went up only 1%. A month ago, the Company released the following PR .

While admittedly the announcement would have had a bigger impact had the company put a potential dollar value on the agreement, the short-sellers and detractors blathered over the Internet that it was just a “Framework Agreement” and would never go anywhere. They are either in denial or purposely hiding the truth. Just like the initial agreements signed with Geely, each of the initial agreements for the three different manufacturing facility “builds”, along with the Alibaba/ZTE/UBER etc.; and most all other initial agreements to include the addition of the newer 16 CarShare Cities, they all start in China as “Framework Agreements”. But this is NOT the first Agreement entered into by KNDI with Pang Da. The last one not only reached its short term goal, but in fact doubled it in about 45 days. Let’s look at the original agreement first.

Note the commitment was for Pang Da to take 1000 KNDI EV’s by year end or a little over a month from the PR. Did they do it? You bet and more. They sold 2,000 KNDI EV’s by year end as per the below KNDI Jan. 26, 2016 PR .

Now let’s look at how the Pang Da deal was discussed on KNDI’s Q2 Conference Call when I brought up the subject. Mr. Hu does not speak English so KNDI IR head, Kewa Lou is doing the translating.

As you can see, Hu is quite confident that Pang da will take at least the 60,000 EVs for the College Program alone. As he alludes, it is not a lot of cars considering that Pang Da is running this program for college campuses Chinawide. But even more important in this discussion is his confirmation that KNDI and Pang Da already have an agreement allowing Pang Da to (non-exclusively) represent KNDI branded vehicles across China. As I mentioned on the CC, for Pang Da to add an additional 60,000 retail sales over the same period of time, it only takes one EV sold per month per location. So I would expect much more than 60,000 additional consumer units over the same time frame

But let’s look at another interesting point at the end of this CC segment. The comment about discussing a partnership with Hengxin. In June, an article in China appeared with a lot of pictures headlined:

Now one might think KNDI, who has not mentioned exporting any EV’s in an announcement would find this Viet Nam situation newsworthy if stock promotion was a priority. But the response I got from the Company was; “Yes, it is KNDI branded EVs, but KNDI is not the one exporting. KNDI is just selling to distributor and he can do whatever he wants with the EV”. Not a surprising answer to those who know how conservative Chairman Hu is.

In just the past 24 months the JV has sold some 40,000 PEVs, with over 30,000 now in the World’s largest CarShare program.

In late 2013, I paid a second visit to KNDI in Hangzhou, China, a city with a population of 9 million, just after the joint launch of KNDI and its affiliate, ZZY’s first City CarShare (Micro-bus) program. At that time there were approximately 1000 KNDI EV’s available for turnkey hourly rental, including insurance, for around $3.20 an hour. Even in so large a city, every hour or so, I would see one of KNDI’s little green and white EV’s traveling the streets. Today, Hangzhou alone has some 18,000 KNDI EV’s and with the massive expansion announced late last year of the KNDI/ZZY program to some 15 additional Cities with total population over 220 million, the Program had already passed 30,000 EV’s by Q1.

Next week the G20 Summit is being held in Hangzhou. I would imagine KNDI’s/ZZY Micro-bus fleet will be hard to miss by these World leaders.

In Q2 16 alone, not included in the 30,000 KNDI reported an additional 4500 EVs were sold to the Micro-bus mainly in new cities.

On a World scale, just how big is this CarShare program? Well, Avis owned ZipCar (ZIP) claims to be the World’s largest CarShare with over 12,000 cars. In Jan 2013 Zip Car was bought by Avis for $600 million including debt . At that time they had 9,000 cars in their fleet with about 6000 owned, the rest leased. ZIP which was public at that time had YE 2012 earnings of $15.5 million . I bring this up for perspective.

While KNDI only owns 9.5% of ZZY, it is the sole supplier of its cars which are bought by, not leased to ZZY. As you can see, Micro-bus is already 2.5 times larger than ZIP and growing at a 100%+ rate compared to ZIP at under 10%. The beauty of KNDI/ZZY Business Model for KNDI is that it’s EV sales growth to KNDI from Micro-Bus will continue to be exponential not only by selling additional EV’s to the program, but also by selling replacement EVs as the older cars are taken out of service. So think about it. Almost like “razorblades”.

If Avis bought ZIP for twice KNDI’s current market cap, how ridiculously undervalued is KNDI just from the detractor/short-seller, much-maligned Micro-bus program alone?

Conclusion

I am sorry I had to make this article so lengthy to hopefully “get the point across” on just how incredibly undervalued KNDI is by any known valuation metric. But as you note from the lead-in summary and comments throughout the report, I have is a two-fold reason for this writing. A week ago, KNDI was attacked in print by an amateur short-seller who for the third time in 19 months took advantage of SeekingAlpha’s broad Internet exposure and lax attitude of letting anyone write anything, the truth be damned. Due to his “catchy” headline, “ Kandi Technologies: Chinese EV Clunker Begins To Break Down Amid Subsidy Scandal, 70% Downside ”, and 95% fabricated accusations within, needless to say, the stock suffered a 7% down day and continues to suffer from the lies and innuendos throughout his rant. While some might wonder why the Company doesn’t challenge such trash, I am in agreement with the Company that they ignore him. Fore by doing so, particularly with such a light-weight as this “target fixated” writer, whose whole portfolio of attack articles has been only against KNDI, it will only give him an ego boost. So without the Company’s awareness, I have taken these last several days to compose my own challenge to his lies and disinformation. Not just rhetoric, but clear rebuttal with back-up links, either in English or Translated from China. While I can give him no credit for moral compass, I can give him credit for being an expert on the “Big Lie” theory. That being; if you say something “So Bold, Outrageous and in an Affirmative Manner, honorable people would just assume it Must Be True”.

As mentioned. Throughout my report, I have addressed a number of his lies and innuendos if appropriate within the frame of just recent KNDI developments. Below, I will make an opening comment then address the few additional lies outside that scope that were so egregious that I feel must also exposed. But I will limit it to only the most significant.

Comment Regarding Attack Article

Let me first say that over my eight year ownership of KNDI stock, I have closely read some 50 published attack articles over the last six years against KNDI dating back to 2010. While perhaps more immune to “sensationalism” then the average shareholder due to my financial background, like any shareholder, I approached each of these article with nervous apprehension that “maybe this writer knows some concerning issue that I don’t”. Over the years, while I have learned there is no limit to the extent some low-level attack writers will stoop, there has been a positive side. The attacks have forced me to expand my own due diligence and knowledge about the Company which in the end result has consistently led to the same conclusion. “Much ado about nothing”. But on a positive side, I not only gained more knowledge of the Company than I ever would have expected; I also came away with the solace that KNDI’s brilliant CEO, a true China EV Pioneer going back to the early 2000’s when appointed as PEV Chief Scientist of China’s National 863 Plan and winner of China’s 2014 Green Car Innovator of the Year award Hu Xiaoming, is the perfect and honest steward for KNDI and its shareholders.

In the past, short sellers and their internet agents, most with long professional track records of attacking myriads of stocks, while attempting to spin certain observations by opinionating to the negative, had never once used the word “fraud” against KNDI in their writings. They did their job of raising suspicions and as time has passed and their reservations have proved inconsequential, they have moved on to other issues. However, the author of this last attack article, whose total portfolio of such writing has been against KNDI, has in my opinion gone too far to just ignore. In his most recent article he used the word “fraud” 12 times. In his January 6, 2015 article “Kandi Crushed: Mary Jo White's " Broken Windows" Policy Makes An SEC Enforcement Action Inevitable ” the word “fraud” shows up an incredible 48 times! Needless to say, to invoke the full name of the head of the Securities and Exchange Commission in such a headline stating the inevitability that the SEC would find serious problems with KNDI would be unnerving to most investors. To bring thing into better perspective, let me revisit the 2013 SEC investigation of KNDI he was referring to with the Broken Windows article.

While maybe surprising to most, there is no requirement on any Company to publically disclose initiation of an SEC investigation, only a negative outcome. The vast majority of companies don’t. However, KNDI a year prior did to his past article did report its receipt of the opening of an investigation in its public filings. Some six weeks after the “Broken Windows” article appeared, it must have been demoralizing to the author learn in a press release from the Company that the SEC ended its investigation. With this revelation, not only was the “Enforcement Action” off the table, but unlike most SEC investigations that typically stay open for years, KNDI actually reported receipt of a letter from the SEC informing KNDI in writing that the investigation was concluded with no findings against the Company . I state “demoralizing” since this author has been silent in his writings against KNDI for 15 months until his most recent article. I bring this up to remind readers that some of the more serious accusations in his recent article were made well before the start of the SEC investigation and were cleared during

Remember, most of the derogatory points of the attack article have already been addressed piecemeal in my article above. Let me just finish this by first reproducing the writer’s opening “bullet” Summary in his recent article and address as appropriate in italic print.

Summary (From the Attack Article)

* Kandi has found itself at the center of major subsidy scandal that has rocked China's nascent EV industry

This all covered and debunked in my article body.

* Kandi's auditor resigned in April 2016 after being banned by the PCAOB for failure to follow up on what we believe are blatant signs of fraud by KNDI's management.

This old news which has been around the net for over three months is true in part. The Company’s old Auditor has been fined $10,000 and banned for a year before being allowed to recertify. A good portion of the reason behind his penalty was for giving improper advice to KNDI Management in a few instances from 2010 to 2012. The irregularities were uncovered by the SEC in the 2013-2014 SEC KNDI Fact Finding Investigation and turned over to the PCAOB. Whatever irresponsibility that was discovered by the SEC against KNDI, obviously did not raise to the level that required SEC action against the Company since the SEC you know from the prior section that the Commission ended its 14 month investigation finding no action required against KNDI in early 2015. Perhaps there was no way for the attack writer to have known this, or just didn’t care, so maybe he could be excused. But what he can’t be excuse for is claiming the Auditor Resigned which is not true. The Auditor was Dismissed by KNDI before the findings and

replaced by the highly respected International Accounting Firm BDO

. If one were to believe the author, KNDI is still operating without an Auditor since for whatever reason, BDO’s name is found nowhere in his report.

* Geely Automotive dumps its 50% stake in Kandi joint venture, citing surging losses and policies issued by government negatively affecting KNDI's eligibility for subsidies.

This all covered and debunked in my article body.

* Past six quarters show balance sheet deterioration accelerating rapidly while Kandi continues to burn cash and pay management outrageous stock-based compensation.

This all covered and debunked in my article body.

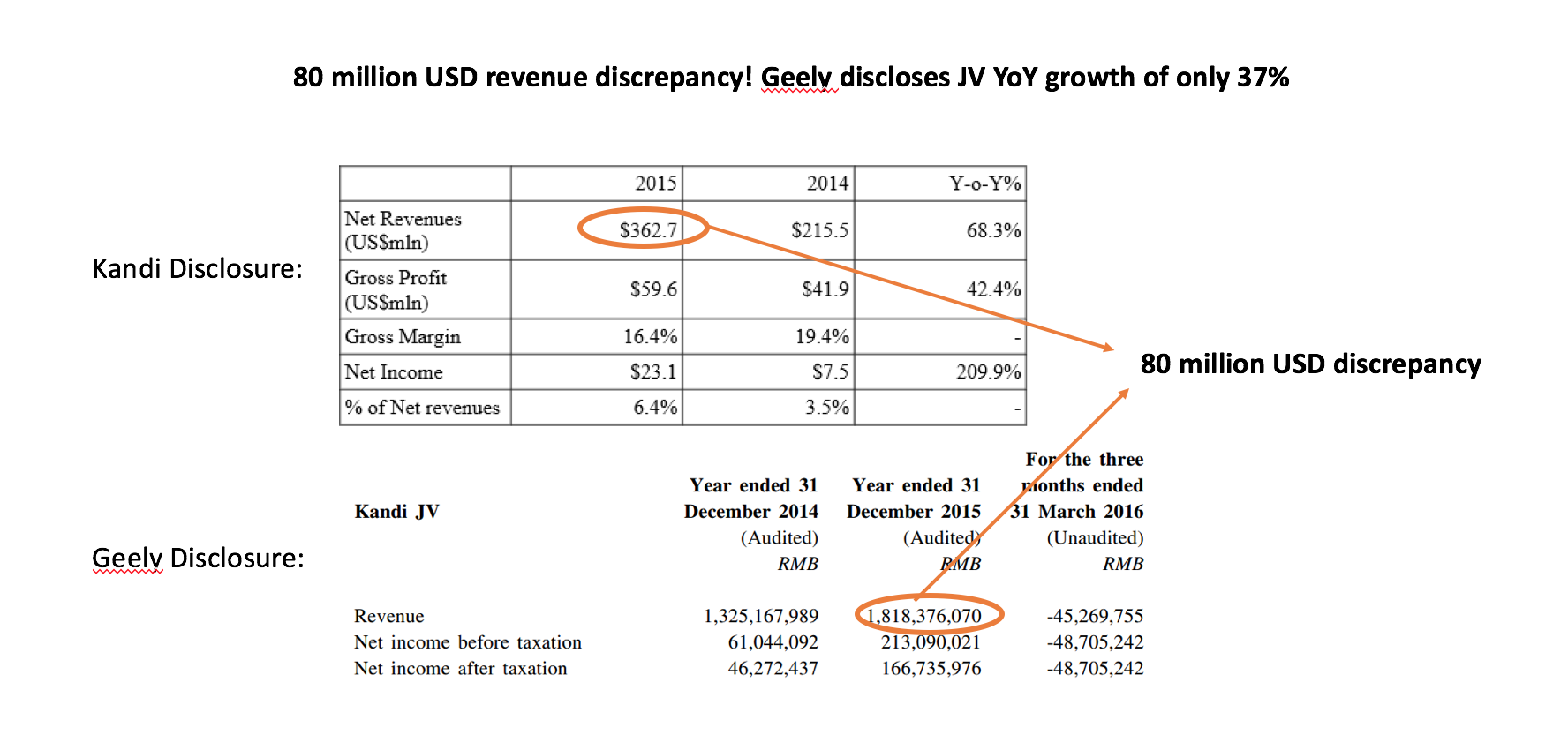

* Panama Papers leak revealing intentional concealment of self-dealing transaction by chairman and an unexplained $80 million discrepancy between Kandi and Geely filings raise serious risk of delisting and SEC investigation.

Herein lies a “Big Lie” regarding the Panama Papers” (which based on my recent calls from even long time investors, seem to have caused the most concern from his article. He also mentioned a small lie about the $80 million discrepancy. Let’s do the $80 million difference first.

This cute graphic he made and could have been a “dramatic” revelation if it meant anything. As I discussed above, neither KNDI nor the JV can report full consolidated “numbers”. So each have their respective Auditors put together a very condensed income statement as a footnote in their respective filings. The JV has used KNDI’s auditor, BDO since inception and Geely uses Grant Thornton. It is obvious that the two different auditors must account for certain revenue line items in a different way. But what the author failed to point out was the important Bottom Line. Converting the 166.7 million rmb as reported by Geely using YE Dollar to RMB conversion rates come out the same bottom line for both. If there is an error, I would tend to trust KNDI and BDO over Grant Thornton since BDO is the JV Auditor.

Bogus Panama Papers - As warned above, some of the more serious accusations in his recent article were made well before the start of the SEC investigation. A prime example being the “catchy headlined” non-existent “Panama Papers” given as “shocking evidence” KNDI Chairman had been “outed” with an actionable improper disclosure item. To quote the authors topic heading; “ Panama Papers Expose CEO's Self Dealing ”. The gist supposedly being; The author alone had discovered and was disclosing that at one time the KNDI Chairman was controlling shareholder of a Company, KO NGA, that KNDI ultimately purchased while not disclosing his ownership.

Unquestionably, if true, an SEC violation with likely consequences. However, had the author taken the time to follow-up on his revelation, he could have easily found on the internet that not only was this not a new discovery, but lengthily vetted in a two year prior KNDI attack article as not being the case.

In actuality, KNDI Chairman, an independently wealthy China Industrialist, at one time did own a holding company, KO NGA in his personal portfolio. However as disclosed by the 2012 attack writer, in 2011 KO NGA sold certain of its units assets to others. It was later, in 2012, KNDI acquired one of these units called Yongkang Scrou a maker of EV motors, controllers, auto AC units, generators and other auto parts for approximately $8 million in KNDI stock. As publically stated at the time by KNDI, a “fairness opinion” was sought and received by outside appraisers to come to that value. (I might add at this time that today, a good bit of KNDI’s “part sales” are manufactured by its acquired YS subsidiary).

As I mentioned above, had the author taken a few minutes time to search the internet, he would have discovered that a much higher profiled and proficient KNDI attack writer, Reinvesting, had also vetted this same subject in a Seeking Alpha article , Sept. 2012. In a portion of Geo’s article it was clearly reported that KNDI’s Chairman was an owner of KO NGA, but he was not an owner Yongkang Scrou when acquired by KNDI. It is also important to remind that all this happened less than two years before the start of the SEC investigation, whose investigators had full knowledge of the transaction and could have acted if they felt there was some violation.

To conclude this subject, let me clarify why I said, non-existent Panama Papers revelation. The link provided by the author in his article was NOT to the infamous Panama Papers leak from April of this year which has its own website , it was to the “ Offshore Leaks” database , which has been around since early 2012 but also hosted by the ICIJ. By its own disclaimer, the ICIJ states the Offshore Leaks data is only confirmed up until 2010, while the Panama Papers is up to 2015 . Only the author knows what was in his mind when he made the error of crediting his “discovery” to the wrong database, but since he gave the link to the OL database, perhaps we should assume it was a simple error while hurriedly trying to get his article out. But with such an important error, what does this say about the rest of his accusations?

Author Disclosure: I Own Common Stock and Public Options in KNDI