Emerging Markets Debt: 4 Questions for Investors

The emerging markets (EM) debt investable universe is large, diverse, and often misunderstood. While it offers the potential for higher returns, it also comes with higher risks. To unlock alpha opportunities, it’s important to have a full understanding of this unique asset class.

Comments are edited excerpts from our continuing education series, Understanding Emerging Markets Debt. Learn how to earn CE credits now.

What is EM Debt?

The EM debt investable universe is composed of fixed-income securities issued by EM governments and companies. Overall, EM debt consists of 900 issuers from more than 90 countries.

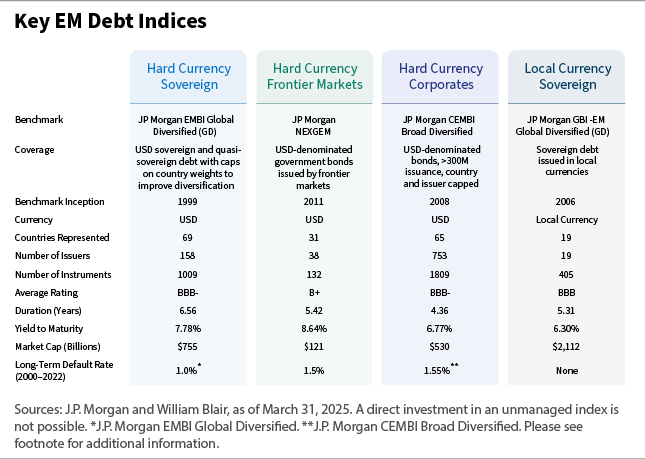

Securities can be issued in hard currencies or local currencies, and there are four universes within EM debt: hard currency sovereign debt, hard currency frontier markets debt, hard currency corporate debt, and local currency sovereign debt.

Hard currency debt is denominated in developed-market currencies (such as the U.S. dollar), issued in international markets, and subject to the issuing country’s laws. On the other hand, local currency debt is denominated in EM currencies (such as the Brazilian real or the Mexican peso) and predominantly issued in local markets under the issuing country’s laws.

In addition, sovereign debt is issued by a national government to finance its activities or manage its debt and is tied to a country’s fiscal health and political stability. Corporate debt is issued by corporations to raise capital for business operations and depends on the financial strength and profitability of the issuing company. One can also further narrow both of these categories down by focusing on frontier markets debt, which is issued by governments or corporations in frontier markets; these are economies that are less developed than emerging markets but have high growth potential.

EM debt is often tracked and analyzed through various indices, which serve as benchmarks for both hard currency and local currency debt. One of the most prominent indices for hard currency EM debt is the J.P. Morgan EMBI Global Diversified. For local currency debt, the J.P. Morgan GBI-EM Global Diversified is widely used.

These indices are crucial for investors as they provide a framework for measuring performance, assessing risk, and making informed allocation decisions within the EM debt universe. And inclusion in these indices often signals a certain level of credibility and market access for the issuing countries, which can influence investment flows and borrowing costs.

Why Invest in EM Debt?

EM debt is a sizable asset class that has substantially grown over the years. It now represents close to a quarter of the global fixed-income universe, and is diversified across countries, currencies, and corporate credit issuers.

From a credit perspective, we believe EM debt appears solid, with strong fundamentals in both sovereign and corporate credit when compared to similar issuers in developed markets. Multilateral and bilateral institutions, such as the International Monetary Fund (IMF), provide strong support via accessible and affordable financing for EM countries as well. This helps contribute to lower default rates, as countries can secure stable funding even in unfavorable market conditions.

EM debt now represents close to a quarter of the global fixed-income universe, and is diversified across countries, currencies, and corporate credit issuers.

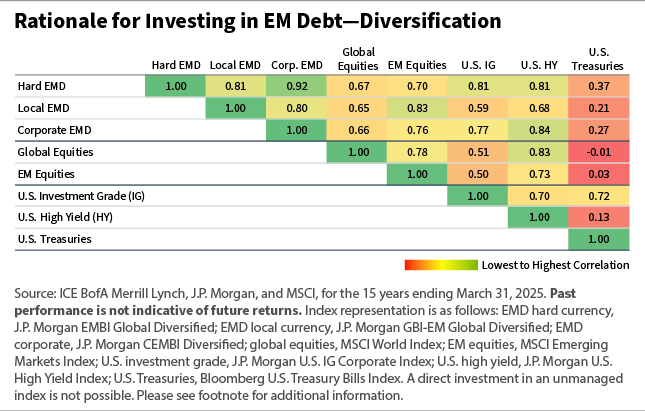

In addition, EM debt has tended to have a lower correlation to other global asset classes, which may offer investors the potential for diversification.

However, EM debt is often misunderstood, and therefore under-owned and undervalued, in our opinion. Several factors contribute to this: perceived risk vs. actual risk, underrepresentation in global fixed-income indices, inefficient pricing, and historical biases.

We believe this misunderstanding creates potential opportunities for investors who can recognize the asset class’s true strengths and potential for alpha generation.

What are Performance Drivers of EM Debt?

We believe performance of EM debt is primarily driven by two forces: global economic growth and global liquidity conditions.

Improving economic conditions can lead to fundamental improvement in EM countries, which can result in lower risk premiums. And when global interest rates are low and global liquidity is abundant, we have seen EM debt perform well at times.

In market environments with declining inflation or falling interest rates, EM debt has also performed well, as it has tended to display a higher sensitivity to rates. In volatile market environments, EM debt has typically displayed higher volatility than other fixed-income asset classes in the developed market space due to rising risk aversion and investor outflows. But this asset class has historically performed well after periods of high market volatility.

In addition, we believe the U.S. dollar plays an important role in EM debt, and securities may benefit when the U.S. dollar depreciates.

We believe this misunderstanding creates potential opportunities for investors who can recognize the asset class’s true strengths and potential for alpha generation.

What are Common Myths About EM Debt?

Investing in EM debt is often viewed through a lens of caution and underscored by a common narrative that emphasizes perceived heightened risk. One common myth about the asset class is, “EM debt isn’t right for my investment portfolio,” as some investors often avoid EM debt because of concerns over risk, volatility, and lack of familiarity.

However, we believe this myth, among others, tends to overshadow the nuanced realities of EM debt, and dissecting them reveals an asset class that, when navigated with insight and expertise, presents compelling opportunities for discerning investors.

Marcelo Assalin, CFA, partner, is the head of William Blair’s emerging markets debt team, on which he also serves as a portfolio manager.

Want more insights on the economy and investment landscape? Subscribe to our blog .

The J.P. Morgan U.S. High Yield Index measures the performance of U.S.-dollar-denominated below-investment-grade corporate debt publicly issued in the U.S. market. The J.P. Morgan U.S. Investment Grade Corporate Index measures the performance of U.S. investment-grade corporate debt. The J.P. Morgan CEMBI Broad Diversified Core Index tracks the performance of U.S-dollar-denominated bonds issued by emerging market corporate entities. The J.P. Morgan GBI-EM Global Diversified Index tracks local currency bonds issued by emerging market governments. The J.P. Morgan EMBI Global Diversified Index tracks liquid, U.S. dollar emerging market fixed- and floating-rate debt instruments issued by sovereign and quasi-sovereign entities. The J.P. Morgan NEXGEM Index tracks U.S. dollar-denominated government bonds issued by frontier markets. (Index information has been obtained from sources believed to be reliable, but J.P. Morgan does not warrant its completeness or accuracy. The indices are used with permission. The indices may not be copied, used, or distributed without J.P. Morgan’s prior written approval. Copyright J.P. Morgan Chase & Co. All rights reserved.) The MSCI Emerging Markets Index is a free-float-adjusted market capitalization index that is designed to measure equity market performance in global emerging markets. The MSCI World Index is a market-capitalization-weighted index of stocks from companies throughout the world and is used as a common benchmark for “world” or “global” stock funds intended to represent a broad cross-section of global markets. The Bloomberg U.S. Treasury Bills Index measures U.S.-dollar-denominated, fixed, rate, nominal debt issued by the U.S. Treasury.

Index performance is provided for illustrative purposes only. A direct investment in an unmanaged index is not possible.

The post Emerging Markets Debt: 4 Questions for Investors appeared first on William Blair .